Current Funding Environment

Wednesday’s inflation print showed a March increase of 0.1% versus February and a year-over-year increase of 5.0%, both of which were better than expected. Markets rallied following the news, at least until the specter of recession caused a reversal of equity gains. The game remains the same: markets want easy money and inflation plus unemployment plus recession equals Fed policy and interest rate levels. Memories of the long 1970s slog through declining and then accelerating inflation levels suggest that it’s too early to declare victory (5.00% is still a long way from the Fed’s 2.00% target range). Nevertheless, hopes increased that the Fed may truly be at or very near the end of its tightening cycle.

|

1 Year |

5 Year |

10 Year |

30 Year |

|

|

April 14 —UST |

4.82% |

3.61% |

3.52% |

3.74% |

|

v. March 31 |

+19 bps |

-1 bp |

+2 bps |

+5 bps |

|

April 14 –-MMD* |

2.36% |

2.08% |

2.10% |

3.18% |

|

v. March 31 |

-13 bps |

-14 bps |

-17 bps |

-12 bps |

|

April 14 —MMD/UST |

48.96% |

57.62% |

59.66% |

85.03% |

|

v. March 31 |

-4.82% |

-3.71% |

-5.20% |

-4.40% |

|

*Note: MMD assumes 5.00% coupon |

||||

SIFMA reset this week at 2.17%, which is approximately 44% of 1-Month LIBOR and represents a -180 basis point adjustment versus the March 29, 2023 reset.

Unsustainable Trends

The web version of The Wall Street Journal got rid of its special section on the “2023 Bank Turmoil,” which is a sign that we’re past the worst of this chapter in the Dickensian saga in which our financial system hero navigates all sorts of unfortunate characters and events in search of a new “normal.” Banking distrust ripples continue, with various clients sharing the work they are doing to peel back layers of counterparty risk to understand whether threats loom in downstream financial dependencies. Our regulatory infrastructure has shown itself to be a mile wide and an inch deep, which fuels the kind of skepticism about the reliability of designated watchdogs that leads to self-directed risk assessments.

At one level, this is a helpful and important exercise. The credit and financing structure of any complex healthcare organization is just another supply chain, and it is good to understand how yours works and whether there are vulnerabilities that should be investigated. But it is equally important to assess whether the progression of COVID to inflation to Silicon Valley Bank has caused your organization to drift from risk management into retrenchment. Organizations naturally migrate along a risk continuum as they shift between prioritizing returns or resiliency. The important question isn’t which of these bookends is right, but rather what shapes the migration; the defining event is the journey, and the critical Board and C-suite conversation is whether your risk management program is enabling or constraining future growth.

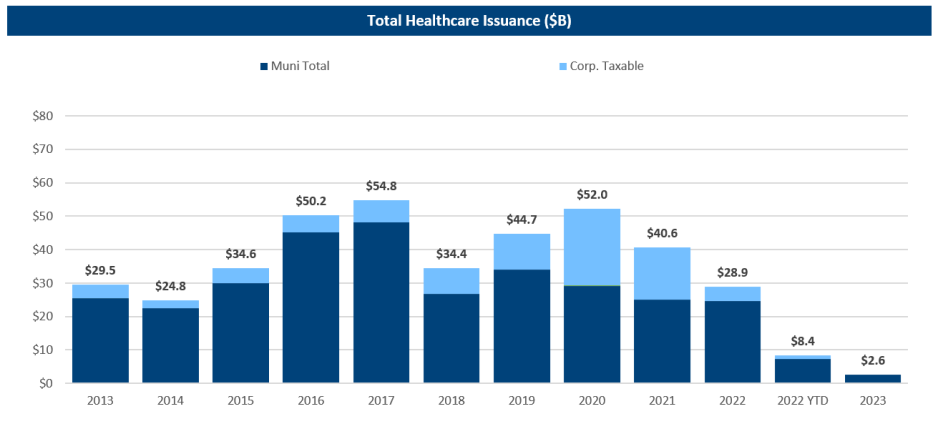

We continue to monitor the extraordinary decline in not-for-profit healthcare debt issuance. Sources we rely on show healthcare public debt issuance through Q1 2023 down almost 70% versus Q1 2022. Similar data sources aren’t available, but anecdotal input from our team suggests a comparable drop-off in healthcare real estate as well as alternative funding channels. At the same time, although margins have recently improved, operating cash flow across the sector has been weak over the past 12-18 months. If capital formation from internal and external sources is a sign of vibrancy, healthcare is listless.

Source: Thomson Reuters, MuniOS as of March 31, 2023; Bond Buyer as of March 31, 2022

The primary culprit isn’t rates; the sector has raised capital in much higher rate environments with fewer financing channels (including most of the pre-2008 era). Instead, the rationale most frequently advanced is concern about the reaction from key credit market constituents during this time of unprecedented operating disruption. Of course, this makes sense, but sitting underneath this basic rationale is the question of what might be called “capital deployment conviction.” Long experience confirms that organizations armed with a growth thesis they believe in aren’t shy about “selling” their story to rating agencies and investors and are willing to suffer adverse outcomes on rates, ratings, or covenants, if that is the price of growth. This isn’t happening right now, which introduces the troubling idea that issuance trends are about much more than credit management.

No matter the root cause, recent capital formation is not sustainable. Good risk management leads to caution in challenging times, but being too careful elevates the probability that temporary problems become permanent. $2.8 billion in quarterly external capital formation ($11.2 billion annualized—pause and let that annualized amount sink in) is not sufficient to maintain the not-for-profit healthcare sector’s care delivery infrastructure, especially when internal capital generation is equally anemic. But introduce any competitive paradigm and the underinvestment that accompanies this level of capital formation becomes a harbinger of hard times to come. To riff on Aristotle, capitalism abhors a vacuum, and organizations looking to avoid rating pressure today may be elevating the risk of competitive pressure tomorrow; and it is easier to cope with and eventually recover from rating pressure than it is to confront the long-term consequences of well-capitalized and aggressive competitors. Retrenchment might be the right risk management choice in times of crisis, but once that crisis moderates that same strategy can quickly become a risk driver.

Machiavelli, Sun-Tzu, Napoleon, George Washington, and other great tacticians all advanced some variation of the idea that “the best defense is a good offense.” In the world of risk response, this means that the better choice isn’t to de-risk and hibernate but rather to continuously reposition available risk capacity so that you keep the organization moving forward. Star Trek’s philosopher-king Captain James Tiberius Kirk captured the sentiment best when he said, “the best defense is a good offense, and I intend to start offending right now.”

While getting back on the capital horse is important, clearing rates, relative value ratios, risk premia, and flexibility drivers have all reset over the past 12-18 months, so recalibrating a good capital formation program requires reassessment and may lead to very different tactics. This means that a critical step is to get organized around funding parameters: debt versus real estate versus other channels; MTI versus non-MTI; tax-exempt versus taxable; public versus private; fixed versus floating. The other important part of this is gaining conviction about capital structure risk versus flexibility: do you want to retain flexibility at the “cost” of incurring the market risk embedded in short-tenor or floating rate structures or do you want to sell flexibility in exchange for capital structure risk reduction?