U.S. employers have long played a dual role in the health insurance of their employees – both paying for their health insurance coverage and choosing their health insurance options. Traditionally, these two roles have been tied at the hip, but now, ICHRA (individual coverage Health Reimbursement Arrangement) products offer an opportunity to bifurcate that role.

Through ICHRA, employers can pay for employees’ health insurance and/or healthcare without having any role in the selection of their health insurance plans. Depending on the number of employers opting for these products, this heralds a potentially significant shift, with implications for payers, providers, and the U.S. healthcare ecosystem broadly.

Background

Idiosyncrasies of the tax code brought a large section of US employers into healthcare in the 1940s. Unable to offer wage increases during World War II, employers started paying for healthcare/health insurance as an alternative to offering wage increases to employees. Over time, employer-sponsored health insurance became a mainstay of American life. As healthcare costs have grown significantly, employers have lately been more willing than ever to consider cost management options that they have not seriously considered in the past. However, the last resort option for employers remains deciding not to offers health insurance coverage altogether.

A presidential Executive Order in 2017 changed that dynamic by introducing ICHRAs (launched in 2020) into the healthcare lexicon, products that allow employers to make tax deductible contributions to employees to pay for healthcare without buying or selecting health insurance plan options for them. Depending on the specifics of the arrangements, employees are free to use the dollars in the ICHRA to buy coverage on the health insurance exchanges (HIX) or marketplace and pay for out-of-pocket (OOP) healthcare costs.

Thus, in one fell swoop, the federal government bifurcated the traditional employer role in health insurance.

Now, an employer can offer to pay for employees’ healthcare with tax deductible dollars without the responsibility of choosing health insurance plans and the intricate administrative operations and compliance responsibilities associated with that. For many employers and industry observers, this is the elegant “defined contribution for healthcare” option they have been waiting for, akin to the 401(k) revolution that moved US pensions from a defined benefit to a defined contribution market.

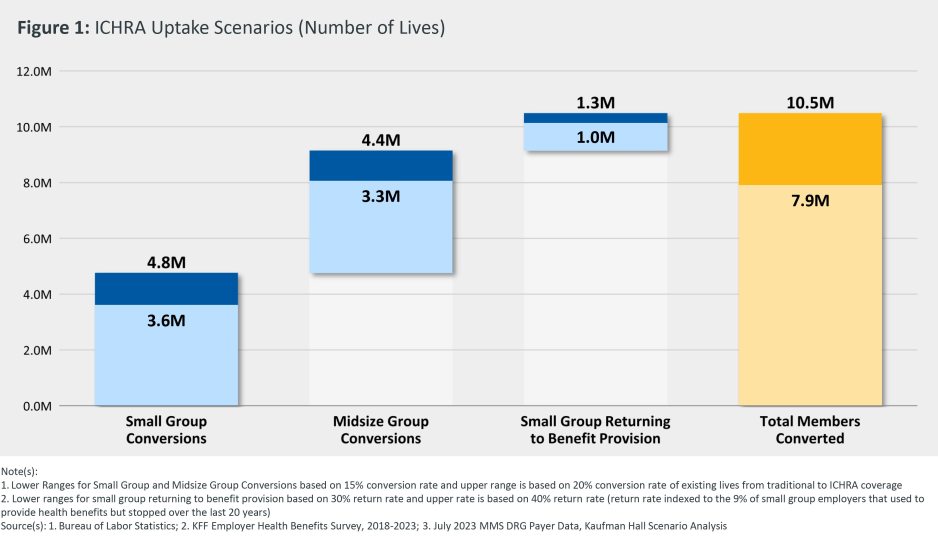

Outlook

The ICHRA market is in a very early stage of evolution, and reliable data on uptake is hard to come by. While still a small market to-date, According to the HRA Council, there has been a 64% growth in the number of employers offering ICHRAs from 2022 to 2023. The Congressional Budget Office (CBO) and Joint Committee on Taxation (JCT) project 2 million lives in ICHRAs by 2032. While there are many uncertainties ahead on how this market will develop (e.g., employer and employee experience with the transition, quality, and stability of the HIX plan options), we believe the market could be a lot larger. Relatively conservative assumptions lead us to believe a scenario of 7-10 million (or more) lives in the ICHRA market is possible in the small and mid-sized group segments of the employer market (without any assumptions made on uptake for segments of employers 250 and above). Figure 1 below shows these scenarios, noting our key assumptions.

In our view, Figure 1 portrays a reasonable scenario, without being overly conservative or optimistic about the ICHRA market. The most optimistic scenario may see the parallels to defined contribution retirement plans that are now held by 48% of private sector employees versus 11% of private sector employees that have defined benefit retirement plans, about 45 years after the 401(k) was first introduced. You don’t need to believe such optimistic long-term scenarios will play out in the ICHRA market (though they might!). Even with gradual uptake, this trend could have significant implications for the healthcare industry.

Implications for Payers and Providers

Payers with a large traditional employer-sponsored health insurance book of business face the classic “Innovator’s Dilemma” as described by the late Prof. Clay Christensen. They are faced with a potentially disruptive force, as ICHRAs convert traditional group business to individual HIX business. Payers with diversified lines of business--including group, HIX and Medicaid coverage--are in a better position, as they have the “catcher’s mitt” to capture conversions out of group business into their HIX plans. However, getting more than their fair share of conversions will require deeper thinking, analytics, and superior execution across all aspects of the payer value chain, especially distribution, provider network, and product design.

Payers without employer group business are in “the catbird seat” as this trend unfolds since they have nothing to lose! They can be highly disruptive to payers with employer group business and capture a disproportionate share of lives as they convert from group coverage to ICHRAs and use the ICHRA dollars to purchase HIX plan coverage. This is a unique, perhaps once-in-a-decade opportunity for a substantial shift of lives from one set of payers in the market to another.

For health systems and other providers, the ICHRA trend represents yet another challenge in the larger ongoing shift in industry payer mix from commercial to government payers. Health systems could find their reimbursements transitioning from the typically higher commercial employer group coverage levels to the lower levels prevalent in the HIX market as employees use their ICHRA dollars to purchase health plans on the HIX market.

On the positive side, for some health systems, this may well be the added impetus needed to urgently pursue alternative business models and cost structures like direct-to-employer models that preserve the attractive employer-sponsored healthcare market, as well as redesign their care models and cost structures to cater to the needs of the new growing but lower per unit reimbursement patient populations.

Conclusion

The ICHRA products are an exciting early trend that will have ripple effects across the payer-provider landscape, with the possibility that some of the more extreme long-term scenarios will radically reshape how healthcare is purchased and delivered in the U.S. However, to get beyond marginal uptake, these products will need to be supported by a broader ecosystem like a mature and stable HIX marketplace, mainstream acceptance of HIX, and convenient price transparency tools to enable individuals to be better stewards of their ICHRA dollars. If this broader ecosystem develops simultaneously with growing employer willingness to convert to ICHRA products, the Great Bifurcation of the employer’s role in healthcare may be here sooner rather than later. Payers and health systems would be well-advised to strategize ahead of this new trend (potentially) achieving escape velocity.

Note: While this blog has focused on ICHRAs, another related product, the Qualified Small Employer Health Reimbursement Arrangement (QSEHRA), presents many similar characteristics and implications for the healthcare system.

Acknowledgements: The author would like to thank Webster Macomber, Brian Ball, Max Timm, Haydn Bush and Rahul Tanna for their insights, reviews, comments, and research on this topic.