The rules of growth for health systems have shifted substantially in the last year. Our recent article, To the Right Partner, Timing Is Everything, explored urgency and readiness for potential partnerships; this companion examines how organizations define their strategic north star beyond the hospital walls.

In a market where reimbursement pressures and policy uncertainty post-OBBB outpace growth, non-acute partnerships are an emerging area of opportunity offering an agile avenue toward sustainability that demands the same level of clarity of purpose, due diligence, and intentional stewardship.

The lay of the land: market dynamics and challenges

Re-emerging M&A activity

Hospital M&A activity resurged toward the latter half of 2025, re-emerging and thawing after a period of frost post-pandemic. Appetite for partnership remains strong among acquirers and buyer interest endured despite persisting board reluctance. Boards began taking cautious steps forward as visibility improved last year, navigating regulatory and policy changes alongside broader economic and global uncertainty in this election year.

Palpable ripple effects of FTC scrutiny

Ongoing regulatory oversight, however, continues to temper the pace of large-scale acute care M&A, paving the way for a marked shift in activity in adjacent sectors: non-acute, outpatient settings including physician practices, post-acute, senior & home care, behavioral health, imaging and lab, and multi-site service partners.

An emerging opportunity

M&A activity is evolving to meet the moment, as healthcare delivery continues to shift toward non-acute, ambulatory and alternative, lower-cost sites of care due to patient, provider, and payer preferences. Hospital-to-hospital consolidation is adapting to meet the moment at a time when “stacking hospitals” proves less viable under regulatory pressure and diminishing returns.

Systems in the $500M–$3B range are emerging as both targets, consolidators, and innovators, exploring partnerships in niche services, technology enablement, and care-at-home models. While headline-grabbing mega-mergers have slowed, a quiet flurry of non-acute activity—physician group acquisitions, joint ventures, care management alliances—signals transformation happening beyond acute care. This emerging opportunity in non-acute spaces represents a shift to more flexible, lower-risk entry points for growth and integration and becomes a proving ground for partnerships at a time when hospitals and health systems must continually re-evaluate their options and their strategic approach.

The invisible frontier: the rise of non-acute partnerships

Many of the most transformative partnerships are not publicly visible. They are embedded among operational joint ventures, shared infrastructure and aligned physician enterprises—often unannounced, inconsistently disclosed and sometimes restructured rather than completed as headline transactions. The unseen, difficult to quantify activity matters most; it’s where competitive advantage is quietly built. These non-acute partnerships are right-sized, mission-aligned and nimble, integrating service lines and capabilities rather than geography alone. They enable more market touchpoints, allowing systems to learn and iterate faster, and “borrow scale” from high-performing specialty organizations.

| Ambulatory surgery expansion | Ascension is acquiring 250 ambulatory surgical centers from Amsurg to grow its care delivery network as part of a broader strategy to right-size its operational footprint and deliver outpatient surgical care in the community setting. |

| Behavior health capabilities | Baylor Scott & White Health and Geode Health entered a joint venture to increase access to high-quality outpatient mental health services for Texans. Geode Health is a multi-state provider of in-person and virtual comprehensive mental healthcare, helping Baylor Scott & White Health address a key pain point for their patients: timely access to behavioral care. |

| Urgent care expansion | University of Pittsburgh Medical Center and GoHealth entered a joint venture to expand urgent care in Pennsylvania and West Virginia with 81 state-of-the-art UPMC-GoHealth Urgent Care centers. |

| Lab capabilities | Corewell Health and Quest Diagnostics entered a joint venture to expand laboratory services in Michigan, introducing lab management, supply chain optimization, blood and anemia programs, and advanced analytics across all 21 Corewell hospitals. |

| Imaging capabilities | BJC HealthCare and Outpatient Imaging Affiliates formed a joint venture to expand diagnostic imaging across greater St. Louis and southern Illinois, supporting BJC’s ambulatory growth strategy by growing its outpatient imaging network and increasing access to retail-oriented imaging services. |

Strategic imperatives for the year ahead

Historically, most non-acute partnerships have been reactive, formed to address underperformance or unsolicited offers rather than embedded in enterprise strategy. Healthcare organizations should take on more proactive recalibration, however. As reimbursement continues to compress, organizations must plan, not react. Recent policy constraints can become margin dilutive, increasing uninsured and underinsured populations, pushing more patients into emergent settings and forcing systems to seek margin elsewhere. A non-acute partnership strategy becomes an important part of an organization’s broader strategic capital planning, responding to competitive forces that siphon higher margin business away from health systems.

The imperative has shifted from scale to strategic, profitable adaptability. Growth for its own sake is no longer enough. Partnerships targeting margin stability, access expansion and capability enhancement are becoming determinant factors in organizational success. Organizations that can realistically reassess organizational readiness and evaluate their financial strength, leadership alignment and governance agility can seize meaningful non-acute opportunities before others.

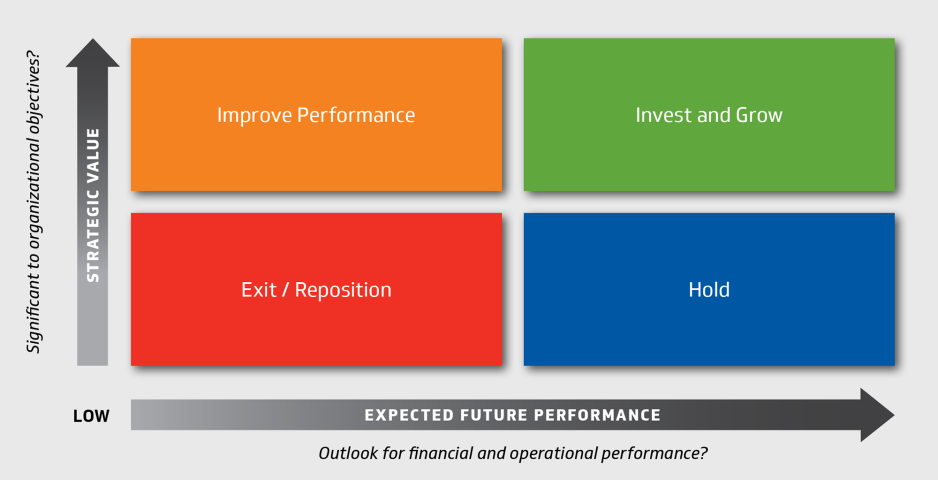

An enterprise Strategic Options Assessment (SOA) of an organization’s business units can be an invaluable opportunity to introduce non-acute scenario modeling and partnership readiness as a recurring, continuous discipline. This approach can help health systems evaluate the capabilities and competences needed to serve their community as they develop a thorough inventory of which core capabilities may need further investment, are missing that can be supported by expert partners, could be more efficient with the support of a partner, and which can be divested or repositioned. For example, a partnership with a skilled nursing facility can help ease post-discharge planning, free beds for patients who are ready to discharge but may lack support at home. A joint venture monetization of outreach laboratory services can raise non-dilutive capital while maintaining access to an essential service delivered at a lower cost to patients.

What’s ahead

Where some organizations once sought size and growing physical footprints, the rules of growth are now different. Organizations must now focus on response over reaction and strategy over scale.

Practical Guidance for Leaders

For executive and board consideration:

- Maintain an enterprise-level discipline for Strategic Options Assessments (SOAs)

Regularly evaluate strategic options across the portfolio, explicitly assessing where non-acute and emerging businesses fit within broader system priorities and strategic goals. - Define a theoretical end state for the system

Articulating what full integration could look like can provide a strategic lens with which future investments are evaluated. - Prioritize capability-building partnerships (tech, analytics, workforce) that future-proof the organization.

Use non-acute partnerships deliberately to accelerate access to technology, analytics, capital and workforce capabilities that meet the needs of the organization and those it serves. - Assess organizational readiness for strategic non-acute partnerships

Evaluate leadership cohesion, governance agility and cultural alignment to execute timely partnership and portfolio decisions. - Maintain awareness of peer activity in non-acute M&A to benchmark timing and approach

Understand how health systems and for-profit players are structuring partnerships and investments to inform timing, positioning and posture.