Hospital and health system transactions

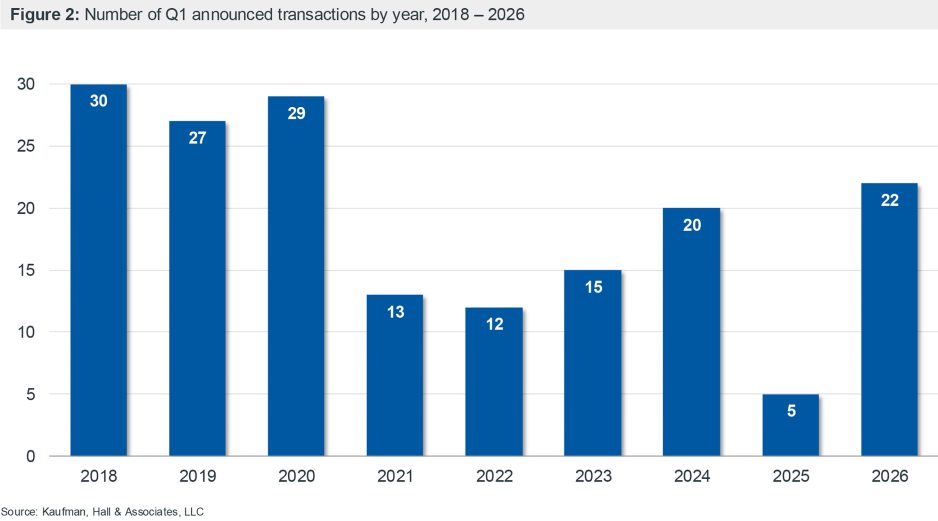

In our 2025 year-end report, we noted building momentum in the pace of hospital and health system M&A transactions over the course of the year, after a period of very low activity early in 2025. That momentum continued into Q1 2026 with 22 announced transactions (Figure 1), a number that outpaced Q1 results for the past five consecutive years (Figure 2).

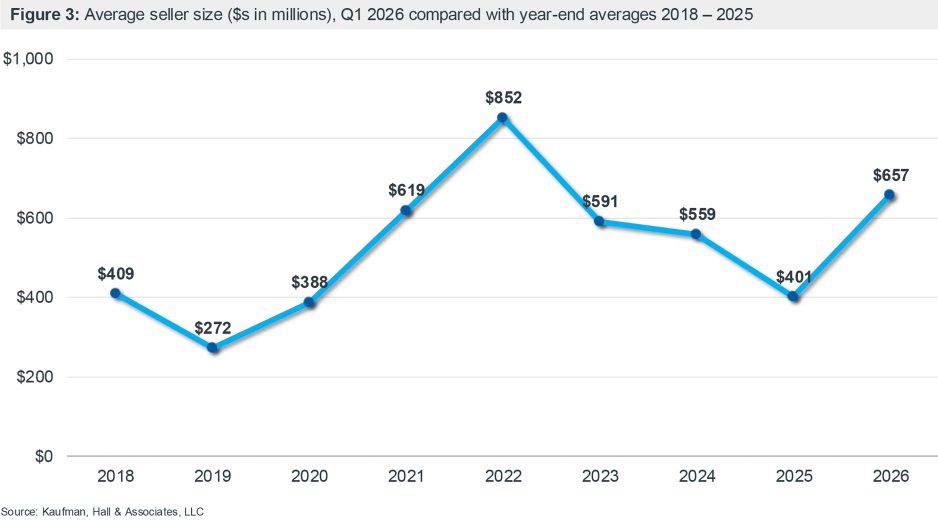

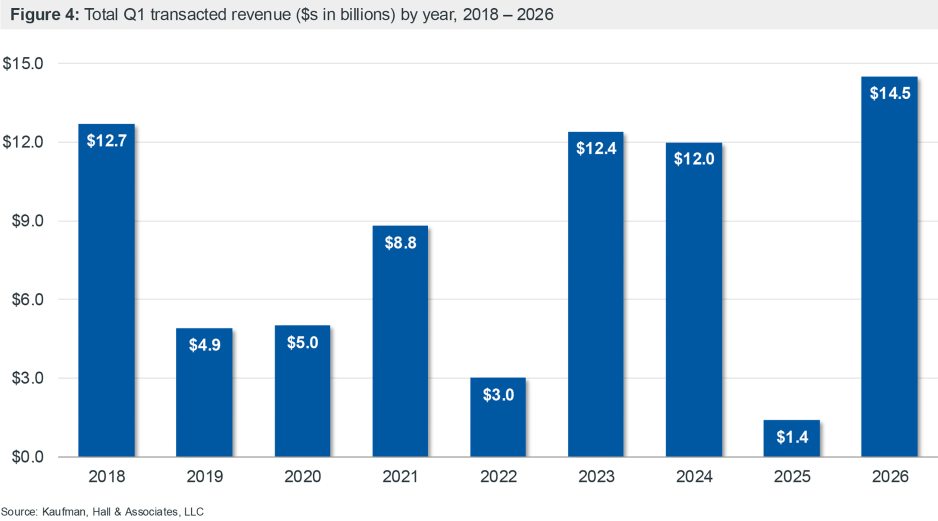

With three “mega mergers” (transactions in which the smaller party has annual revenue in excess of $1 billion) among the 22 announced transactions, both average size of the smaller party and total transacted revenue for the quarter also rebounded. Q1’s $14.5 billion in transacted revenue was the highest Q1 figure we have seen in recent years.

Across the spectrum of Q1 transactions, the signs of strategic repositioning were evident in both continued efforts at portfolio rationalization focused among large and national health systems (both for-profit and not-for-profit) and in the number of independent systems proactively seeking a partner. Divestitures represented 15 of the 22 announced transactions (68%) (Figure 1).

Figure 1: Q1 2026 at a glance

| Number of announced transactions | 22 |

| Average size of seller/smaller party by annual revenue | $657 million |

| Total transacted revenue | $14.5 billion |

| Transactions involving: | |

| Religiously affiliated seller | 3 |

| Governmental seller | 5 |

| Independent not-for-profit seller | 7 |

| For-profit seller | 6 |

| Academic seller | 1 |

| Financially distressed seller | 4 |

| Religiously affiliated buyer | 3 |

| Governmental buyer | 1 |

| Independent not-for-profit buyer | 9 |

| For-profit buyer | 6 |

| Academic buyer | 3 |

| A divestiture | 15 |

Overview of Q1 activity

The 22 hospital and health system transactions announced in Q1 2026 represent a steady recovery in M&A activity that began in Q3 and Q4 2025 (15 and 17 announced transactions, respectively). This is the highest Q1 activity recorded since 2020 (Figure 2).

Three announced mega merger transactions—including the proposed merger between California-based Sutter Health and Minnesota-based Allina Health—helped boost Q1 average seller size to $657 million, in the upper range of recent year-end averages (Figure 3) and the second highest level in recent years.

Higher average seller size and a robust activity level combined in Q1 to produce total transacted revenue of $14.5 billion across the 22 announced transactions (Figure 4), a revenue level that is higher than all of the last eight years.

There was one significant change in buyer/seller dynamics in Q1. While selling activity among for-profit systems remained consistent, buying activity increased significantly. In all of 2025, only one announced transaction involved a for-profit acquirer. In Q1 2026 alone, six of the 22 announced transactions involved a for-profit acquirer (Figure 1).

Q1 highlights

Continued portfolio rationalization

In our 2025 year-end report, we predicted that portfolio rationalization would continue into 2026. Results from Q1 clearly support this prediction, with more than two-thirds of the announced transactions involving a divestiture; by comparison, 45.6% of all announced transactions in 2025 involved a divestiture. Both for-profit and large Catholic health systems announced the planned sale of facilities, including CommonSpirit’s planned divestiture of three facilities to Altru Health System and Providence’s planned divestiture to NorthBay Health.[1]

Factors that can drive divestitures include underperforming markets, inadequate market scale, inability to execute on strategic initiatives, or the need to redirect resources for investment in other core markets or new system initiatives. At the same time, divestitures by large and national health systems have created opportunities for regional health systems to build scale and increase strategic investment within their geographies.

Positioning for the future

The high percentage of divestitures in Q1 is also an indicator of proactive positioning for the future, as systems seek to improve financial performance and balance sheet strength in advance of the anticipated impacts of H.R.1, which are expected to begin materializing in 2027. Another indicator of this proactive positioning is the continued movement of well-positioned independent health systems into strategic partnerships with larger systems.

Some of the most significant examples of independent health systems seeking partners involved health systems of varying sizes that are operating from a position of current strength. Community-based organizations such as Goshen Health are proactively pursuing partnerships to strengthen access to care, services, and specialists.[2] Health systems with significant revenue bases (in excess of $1 billion), such as New Jersey-based Englewood Health, continue to evaluate the scale and capabilities required for long-term success.

“When you’re doing well and neither side is doing it out of need, that’s the best time to partner up,” said Warren Geller, Englewood’s president and CEO, commenting on the system’s decision to partner with RWJBarnabas Health. “Because you never want to be in a situation where you’re making your most important long-term decision under duress.”[3] At the same, the press release announcing the transaction noted the “new challenges” posed by the “changing healthcare landscape,” and Geller stated that, “through this partnership and by combining resources, we will have the ability to greatly enhance the services we provide to our communities in a way in which we would not be able to accomplish alone.”[4]

The return of cross-market mergers?

The biggest transaction announced in Q1 was the planned merger of California-based Sutter Health and Minnesota-based Allina Health, which would create a health system generating approximately $26 billion in annual revenue. Under the plan, Allina would form the Upper Midwest Division of Sutter Health but would maintain the Allina Health name and brand, and a regional headquarters based in Minneapolis. The press release announcing the transaction noted northern California’s leading role in AI and platform development and Minnesota’s position as the leading hub for med-tech and engineering, which could create a system “uniquely positioned to be a national leader in digital and technological advancements that meaningfully improve patients’ and caregivers’ experiences.” [5]

We first called out cross-market transactions as a significant trend in our 2022 year-end report, when the merger of Advocate-Aurora Health and Atrium Health—along with several smaller cross-market transactions—was announced. Will the Sutter/Allina transaction reignite a cross-market merger trend, in which well-capitalized, geographically dispersed health systems come together?

Looking forward

The Q1 2026 trends reflect an industry undergoing transformation. Health systems are repositioning by withdrawing from underperforming or non-core markets, building capital to invest in new capabilities, proactively seeking partners to increase resilience or enhance access to care and services, and placing big bets on new combinations of resources and capabilities. A return to more robust levels of deal-making is a sign that organizations remain well aware of the need to seek combinations and partnerships to face the challenges and opportunities that lie ahead.

Co-authors:

Kris Blohm, Managing Director and Mergers & Acquisitions Practice Co-Leader, kris.blohm@kaufmanhall.com

Courtney Midanek, Managing Director and Mergers & Acquisitions Practice Co-Leader, courtney.midanek@kaufmanhall.com

Anu Singh, Managing Director, anu.singh@kaufmanhall.com

Rob Gialessas, Senior Vice President, rob.gialessas@kaufmanhall.com

Chris Peltola, Senior Vice President, chris.peltola@kaufmanhall.com

Additional contributors:

Nick Bidwell, Managing Director, nick.bidwell@kaufmanhall.com

Nick Gialessas, Managing Director, nick.gialessas@kaufmanhall.com

Nora Kelly, Managing Director, nora.kelly@kaufmanhall.com

Eb LeMaster, Managing Director, eb.lemaster@kaufmanhall.com

For media inquiries, please contact Nancy Matocha at nancy.matocha@vizientinc.com.

[1] Kaufman Hall served as buy-side advisor in these transactions.

[2] Goshen Health, “Goshen Health announces letter of intent to partner with Parkview Health,” press release, Jan. 27, 2026. Kaufman Hall served as sell-side advisor in this transaction.

[3] Jackie Roman, “One of N.J.’s last independent hospitals to join major health chain, 3 years after failed merger with rival,” NJ.com, Jan. 5, 2026.

[4] RWJBarnabas Health, “RWJBarnabas Health and Englewood Health sign definitive agreement,” press release, Jan. 5, 2026.

[5] Allina Health, “Allina Health to join Sutter Health, creating bold vision for nonprofit healthcare,” press release, accessed April 6, 2026.