Hospital and health system transactions

Following a reduced level of hospital and health system M&A activity in Q1 2025, with just five announced transactions, Q2 showed a modest uptick in activity, with eight transactions announced. Approximately half the announced transactions involved divestitures, part of a market realignment process for large regional and national health systems – both for-profit and not-for-profit – that has been going on, and recently accelerating, over the past several years.

Despite this level of activity in hospital and health system M&A through the first half of 2025, other affiliation activity based on transformation and repositioning remains robust. This activity is centered on some of the most significant issues in U.S. healthcare today, including the need for solutions to the mounting crisis in rural healthcare to the ongoing shift in focus from inpatient to outpatient opportunities. In this report, we will highlight some of the affiliation activity occurring outside the area of hospital and health system M&A.

Overview of Q2 activity

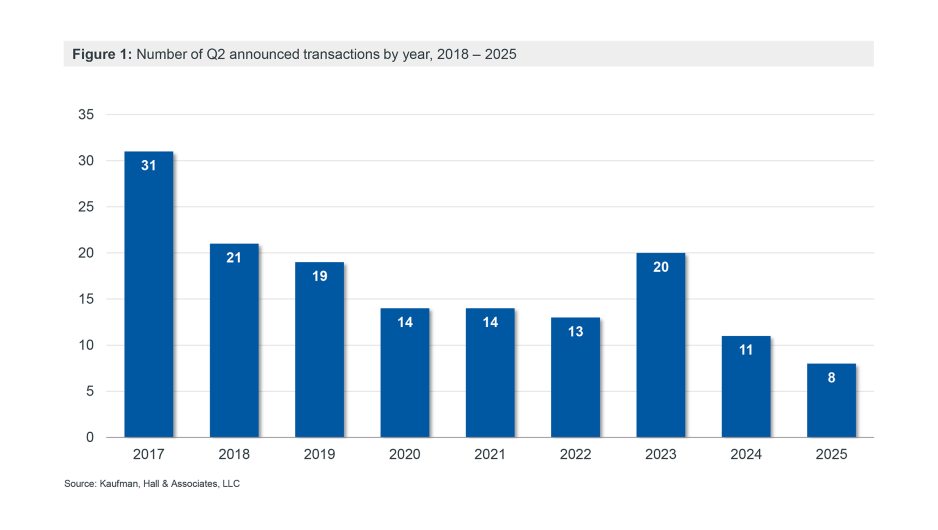

With eight announced transactions in Q2 2025, hospital and health system M&A activity remained low by recent historical averages (Figure 1) but showed an increase over the five transactions announced in Q1.

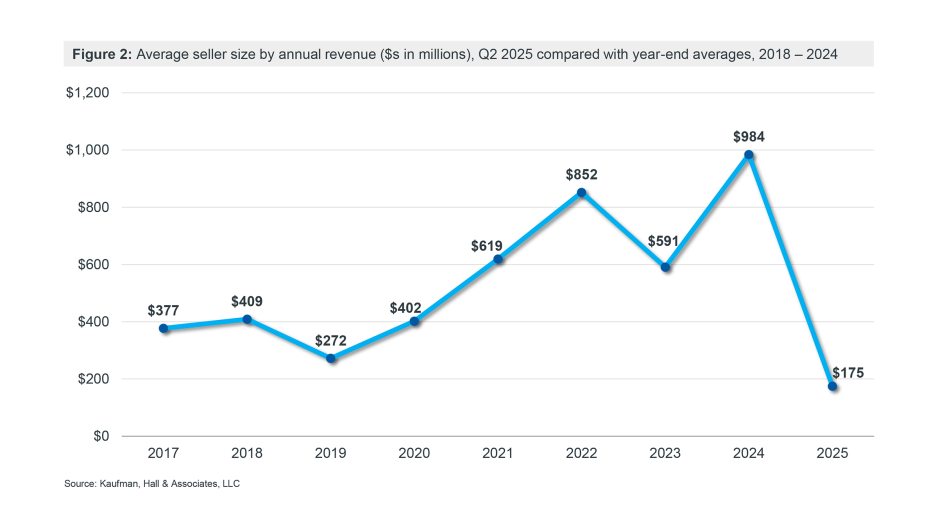

With no mega mergers announced in Q2 (transactions in which the annual revenue of the seller, or smaller party, exceeds $1 billion), and with divestitures of smaller facilities representing approximately half of the announced transactions, the average seller size was a relatively low $175 million (Figure 2).

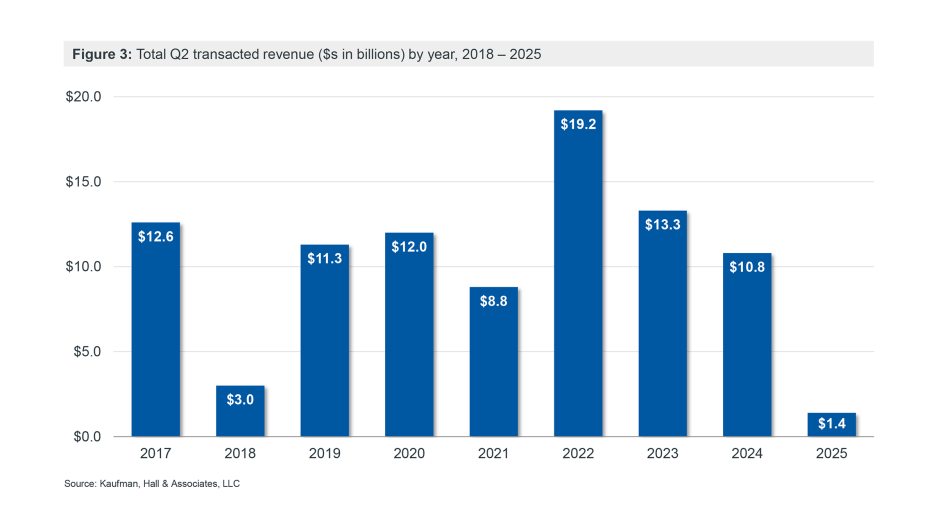

The smaller average seller size, combined with a lower than usual number of transactions, also resulted in a relatively low total of $1.4 billion in transacted revenue for Q2 (Figure 3).

The acquirers in all eight announced transactions for Q2 were not-for-profit organizations. Three of these eight were religiously affiliated and one was governmentally owned. Two of the acquired organizations were for-profit; of the six remaining not-for-profits, three were religiously affiliated and two were governmentally owned.

Q2 highlights

Federal policy impacts on hospitals and health systems come into focus

Hospital and health system M&A activity has been slower in the first half of 2025. Our Q1 2025 report attributed this slowdown to high levels of volatility and economic uncertainty surrounding global trade issues and the potential for significant policy changes affecting healthcare.

With the passage of the One Big Beautiful Bill Act, signed into law by President Trump on July 4, the impact of those policy changes can now be quantified: approximately $1 trillion in healthcare spending cuts over the next decade, with the biggest cuts focused on Medicaid. An article in the Wall Street Journal estimates that nearly 8.7 million fewer people will be covered by Medicaid over the next decade and that Medicaid payments to hospitals will be reduced by almost $665 billion, an 18.2% reduction.

With some of the uncertainty on the economic impact of federal policy changes now resolved, hospitals and health systems have the clarity and visibility needed to refocus their strategy and transformation efforts. This may lead to an interesting dichotomy in health system M&A activity, with the acceleration of organizations looking for partners in response to new financial challenges, but a careful and measured approach being taken by well-positioned health systems.

The future of rural healthcare

Cuts to Medicaid could have a particularly significant impact on rural hospitals, many of which are highly reliant on Medicaid payments. This impact comes as signs emerge of a new effort to address the crisis of rural healthcare.

The financial strains on rural hospitals are evident in Kaufman Hall’s National Hospital Flash Report data. For hospitals with 25 or fewer beds (a category that includes all critical access hospitals), operating margins were down 12.3% year-over-year as of May 2025. The Cecil G. Sheps Center for Health Services Research at the University of North Carolina reports that there have been 196 closures or conversions of rural hospitals since January 2005.

The Rural Emergency Hospital (REH) program, established by Congress in 2021 and available to qualifying rural hospitals since January 2023, represents an effort to preserve access to critical healthcare services in rural communities. Hospitals seeking an REH designation stop providing inpatient services and instead offer emergency, observation and other outpatient services to their community. Approximately 1,500 hospitals could be eligible for REH designation, but participation in the program thus far has been relatively low: as of July 1, 2025, 41 rural hospitals had converted to REH status since January 2023.[1]

Several recent announcements suggest that the REH program may be gaining traction:

- ECU Health in North Carolina has announced a proposal to reopen the shuttered Martin General Hospital as a REH; it is seeking funding for the state to build a new rural care center in Martin County, NC, and to expand inpatient capacity at another ECU location, as the REH would not be able to provide inpatient services.

- In Georgia, Randolph County Hospital has received funding to reopen after a five-year closure; while it will initially operate as a critical access hospital, it plans to transition to a REH.

- In Tennessee, Jellico Regional Hospital – closed since March 2024 – will come under the management of Phoenix Rural Health, which plans to reclassify the hospital as an REH.

- Huntsville Hospital Health System (HH Health) in Alabama announced that it will be assuming full operational and financial control of Lawrence Medical Center. At 98 beds, Lawrence Medical Center is too big to qualify for REH designation. HH Health will be taking a similar approach with Lawrence, however, replacing the hospital with new outpatient facilities and ending inpatient and emergency services. HH Health will seek to expand the acuity of services provided at urgent care locations to help accommodate patients that currently use the Lawrence emergency department. The structure replicates a model HH Health has used successfully in other rural Alabama counties.

The fact that several of these announcements involve the reopening of closed hospitals – albeit in a different form – is a promising sign that different ways of thinking about rural healthcare could help maintain or restore access to essential services and enable a vehicle for such transformation. This trend also suggests that the partners in these transactions believe that there is a viable path forward for rural healthcare.

Moving from inpatient- to outpatient-centered care

One of the biggest transactions announced in Q2 2025 was Ascension’s planned acquisition of AMSURG. The acquisition will add more than 250 ambulatory surgery centers (ASCs) across 34 states to Ascension’s network. This acquisition is not included in the report’s count of announced transactions, as it not a transaction between two hospitals or health systems, but it is representative of much of the M&A activity that health systems are currently pursuing in the non-acute space.

The 2025 Vizient/Kaufman Trends Report identified the need to accelerate bigger, bolder opportunities for better access as one of four trends that should inform hospital and health system strategy. With this acquisition, Ascension has acquired a platform that will enable a pivot to a strategy emphasizing access to convenient, lower-cost alternatives to inpatient care. The acquisition comes as Ascension nears completion of an intentional process of hospital divestitures (Ascension president Eduardo Conrado has noted that “by and large, we’re done with all the major transactions”) , which has enabled investment in both acute and non-acute services to better meet the healthcare needs of the communities it serves.

In a related transaction, Cleveland Clinic announced a partnership with Regent Surgical, which operates and manages ambulatory surgery centers in partnership with health systems in 13 states. In a statement announcing the partnership, Cleveland Clinic CEO and president Tom Mihaljevic noted that “ambulatory surgery centers provide an important setting for health systems to expand access to surgeries, and to be more efficient in the delivery of services.

Looking forward

We anticipate that hospital and health system M&A activity will accelerate, although it may return at a slower pace than it fell, as the industry absorbs the impact of changes resulting from legislative and policy changes. Beyond this specific area of healthcare transactions, however, we see significant activity around new partnerships and affiliations intended to drive the transformation of U.S. healthcare delivery. From rural communities to urban centers, the need for better, more efficiently delivered and lower-cost access to care is propelling and accelerating a shift of focus for nearly all hospital and health system types in the market.

Co-authors:

Kris Blohm, Managing Director and Mergers & Acquisitions Practice Co-Leader, kris.blohm@kaufmanhall.com

Courtney Midanek, Managing Director and Mergers & Acquisitions Practice Co-Leader, courtney.midanek@kaufmanhall.com

Anu Singh, Managing Director, anu.singh@kaufmanhall.com

Rob Gialessas, Senior Vice President, rob.gialessas@kaufmanhall.com

Chris Peltola, Senior Vice President, chris.peltola@kaufmanhall.com

Additional contributors:

Nick Bidwell, Managing Director, nick.bidwell@kaufmanhall.com

Nick Gialessas, Managing Director, nick.gialessas@kaufmanhall.com

Nora Kelly, Managing Director, nora.kelly@kaufmanhall.com

Eb LeMaster, Managing Director, eb.lemaster@kaufmanhall.com

For media inquiries, please contact Haydn Bush at haydn.bush@vizientinc.com.

[1] Hospitals that convert to a REH designation are not included in the Sheps Center’s count of rural hospital closures and conversions.