Hospital and Health System Transactions

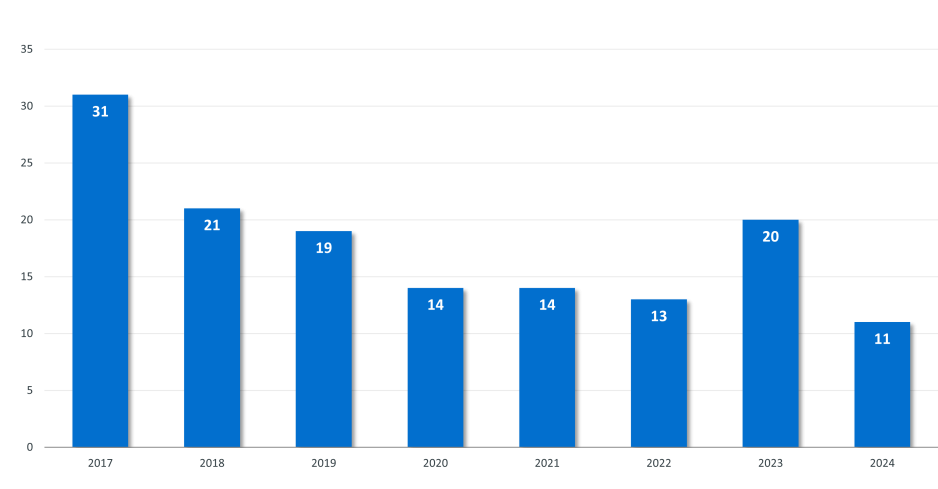

M&A activity in Q2 2024 slowed from a very busy Q1, with 11 announced transactions. Several large transactions in the quarter, however, generated an average seller size by revenue that significantly exceeded year-end averages dating back to 2017.

Two of the 11 announced transactions were “mega mergers” (transactions in which the smaller party has annual revenues of $1 billion or more). Yet neither of these transactions represented a pursuit of greater scale; instead, both were strategic transactions designed, in one case, to gain access to new tools, technologies, and capital investments, and in the other, to support one of the partner’s efforts at system reconfiguration.

Overview of Q2 Activity

The 11 transactions announced in Q2 2024 are below recent Q2 historical averages and represent a pause in the growth of M&A activity we have seen coming out of the Covid pandemic.

Figure 1: Number of Q2 Announced Transactions by Year, 2017 – 2024

Source: Kaufman, Hall & Associates, LLC

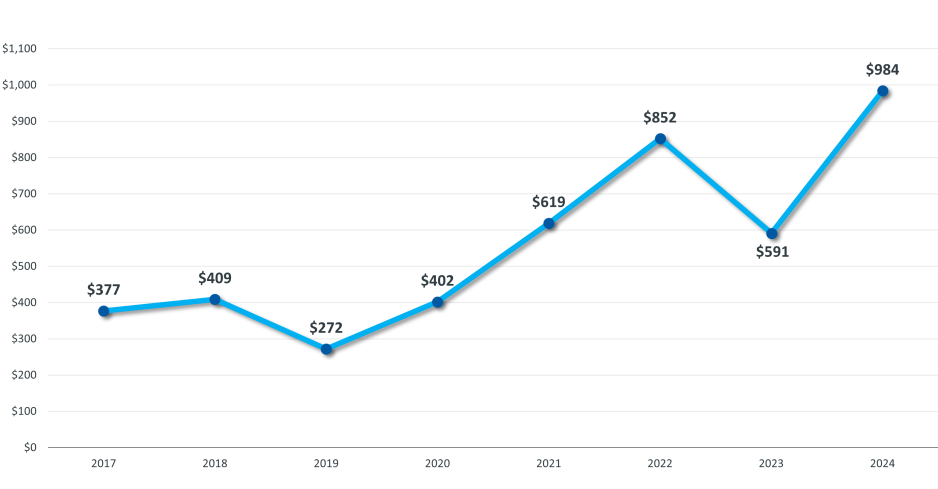

Nonetheless, several very significant transactions in Q2 generated an average seller (or smaller party) size of near $1 billion, resulting in an average seller size for Q2 that far exceeds the year-end seller size averages for every year since 2017 and representing growth in this figure of 161% since 2017.

Figure 2: Average Seller Size ($s in Millions), Q2 2024 Compared with Year-End Averages 2017 – 2023

Source: Kaufman, Hall & Associates, LLC

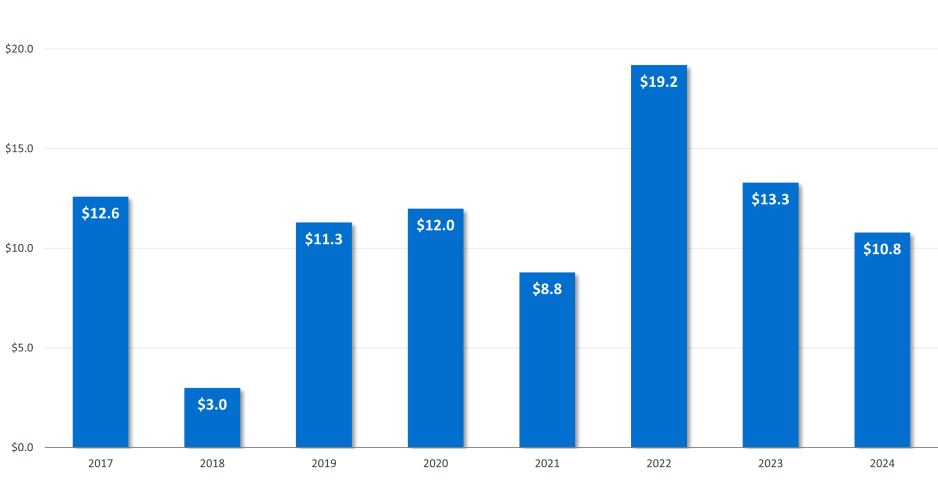

Because of the large average seller size, total transacted revenue for the Q2 2024, at $10.8 billion, also remained near historic levels despite the lower number of announced transactions.

Figure 3: Total Q2 Transacted Revenue ($s in Billions) by Year, 2017 – 2024

Source: Kaufman, Hall & Associates, LLC

Three of the 11 announced transactions involved religiously affiliated acquirers, two involved academic or university-affiliated acquirers, and the remaining six involved other not-for-profit health system acquirers.

For the first time since Kaufman Hall has tracked this data, there were no for-profit health system acquirers in Q2 2024 (excluding real-estate-only transactions). This continues a trend of low for-profit buy-side activity; in Q1 2024, for example, there was just one for-profit health system acquirer in 20 announced transactions.

Q2 Transaction Highlights

An emphasis on strategy over scale characterized the most significant transactions of Q2 2024 and built upon trends we have been commenting on in recent past reports. One trend is the pursuit of intellectual capital and new or complementary capabilities through a strategic partnership, often involving an innovative partnership model. Another trend is the focus of large regional or national systems on market reorganization and strategic realignment of their system portfolios. A third trend is the development of networks involving academic health systems and community hospital partners to sustain and enhance access to care.

A new partnership model takes hold

One of 2023’s biggest M&A stories was Kaiser Permanente’s launch of Risant Health. Risant is a new Kaiser health systems division designed “to spread the very best in population health to diverse markets across the country” by leveraging Kaiser’s expertise in both care and coverage and the capabilities of the systems it acquires. When it was formed, Risant simultaneously announced its first acquisition, Pennsylvania-based Geisinger Health, a transaction that closed earlier this year. With Q2 2024’s announcement that Risant is buying a second health system, North Carolina-based Cone Health (one of the two mega mergers in Q2 2024), it is clear that Risant is on its way to accomplishing its announced goal of acquiring four to five like-minded community-based health systems over the next few years.

Risant’s transactions represent a new model in healthcare M&A, one in which intellectual capital is as—if not more—important than traditional capital. Acquired systems retain their brand, their executive leadership teams, and local governance, but as Cone Health noted in a statement on the benefits of the transaction, the partnership with Risant “brings tools, expertise, and capital to accelerate our charitable mission and strategy.” The ability to launch new services or products, leveraging the expertise of systems that have successfully done the same, is a significant part of the Risant value proposition.

Stability and strength support strategic system realignment

More than 25 years ago, a group of hospitals entered into a joint operating agreement to form BayCare, a health system designed to support not-for-profit healthcare in the Tampa Bay region of Florida. Today, BayCare has reached a level of financial performance and stability that enables it to buy out the interest of Trinity Health, one of its primary investors, and dissolve the joint operating agreement.

This transaction, the second of Q2 2024’s mega mergers, also illustrates an ongoing trend in which large regional and national health systems, both for-profit and not-for-profit, are working to realign their systems to focus on markets with significant growth potential, with divestitures in some markets supporting investments and acquisitions in other markets. In turn, these divestitures enable the growth of regional markets. Other examples from Q2 2024 include Dalton, Georgia-based Hamilton Health Care System’s acquisition of one of Community Health System’s Tennova Healthcare’s hospitals in southeast Tennessee and UAB Health System’s acquisition of Ascension St. Vincent’s sites of care in central Alabama.

Academic health systems preserve access to care

The UAB Health System’s acquisition of Ascension St. Vincent’s central Alabama hospitals and sites of care continues another trend we have been monitoring: the growth of regional care networks centered on an academic health system.

As we noted in our Q3 2023 report, partnerships with community-based health systems can help academic health systems relieve occupancy pressures at their flagship campuses, and also expand opportunities for residency programs, clinical research programs, and patient access to tertiary and quaternary services. But there is another significant function of academic health systems that is often overlooked. Many of them serve as safety-net facilities for their communities, preserving access to care for populations that would be otherwise underserved.

In announcing its planned acquisition of the Ascension St. Vincent’s facilities, which have been in alliance with UAB Health System since 2020, UAB noted that while hospitals are closing across the country, it remains committed to strengthening hospitals in its community. Its acquisition of the Ascension St. Vincent’s facilities, which will be accompanied by investments in their clinical services and infrastructure, will “ensure that [the] community retains access to sustainable, high-quality healthcare” well into the future.

Looking Forward

The pressures to transform healthcare delivery systems are being met with competing pressures from the federal antitrust regulatory agencies, which have taken a more aggressive stance against healthcare M&A activity. But as the focus of transactions moves from scale to strategy, the value proposition for new partnership models intensifies. Transformation of the current healthcare system is a given; the models that will enable that transformation and bring greater value to patients and communities are now taking shape.

Select Transactions in Which Kaufman Hall Served as an Advisor:

Co-contributors:

Anu Singh, Managing Director and Mergers & Acquisitions Practice Leader, asingh@kaufmanhall.com

Nick Bidwell, Managing Director, nbidwell@kaufmanhall.com

Kris Blohm, Managing Director, kblohm@kaufmanhall.com

Nick Gialessas, Managing Director, ngialessas@kaufmanhall.com

Nora Kelly, Managing Director, nkelly@kaufmanhall.com

Eb LeMaster, Managing Director, elemaster@kaufmanhall.com

Courtney Midanek, Managing Director, cmidanek@kaufmanhall.com

Chris Peltola, Senior Vice President, cpeltola@kaufmanhall.com

Rob Gialessas, Vice President, rgialessas@kaufmanhall.com

Media Inquiries: Please contact Haydn Bush at hbush@kaufmanhall.com.