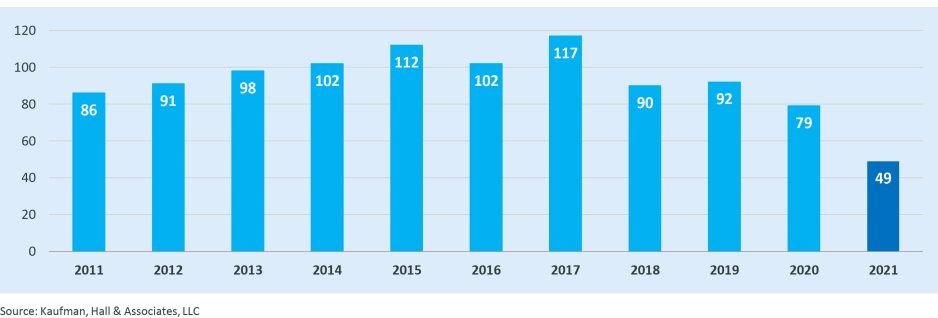

Throughout 2021, there was one consistent trend in partnership, merger, and acquisition transactions between hospitals and health systems: the number of transactions was down, but the size of transactions was up. The process of industry transformation continues as the impact on transaction activity evolves.

As noted in our Q3 2021 report, several factors are driving these changes. There are fewer independent, unaffiliated community hospitals seeking partnerships. Organizations are focused on partnerships with a strong strategic rationale and have become increasingly selective in identifying potential partners. They seek partnerships that will have a transformative impact through the addition of new capabilities, enhanced intellectual capital, and access to new markets or services.

Figure 1: Number of Announced Transactions, 2011 – 2021

One of the major trends we discussed in our 2020 year-end report—a focus on core business strengths—continued into 2021, as did the trend toward strengthening intellectual capital resources, complementing core expertise, and increasing cross-vertical capabilities. Trends we anticipated for the year played out, with a growing diversity of partnerships often focused on attaining deeper and more effective service offerings, as discussed in our Q3 2021 report. We also expect a greater emphasis on partnerships that can help address broader societal issues and the needs of underserved populations.

Following a review of the year in numbers, this report will look first at trends across some of 2021’s most significant transactions, and then discuss what we see as an emerging new phase in healthcare partnerships.

The Year in Numbers

Trends in the data for 2021 include the following:

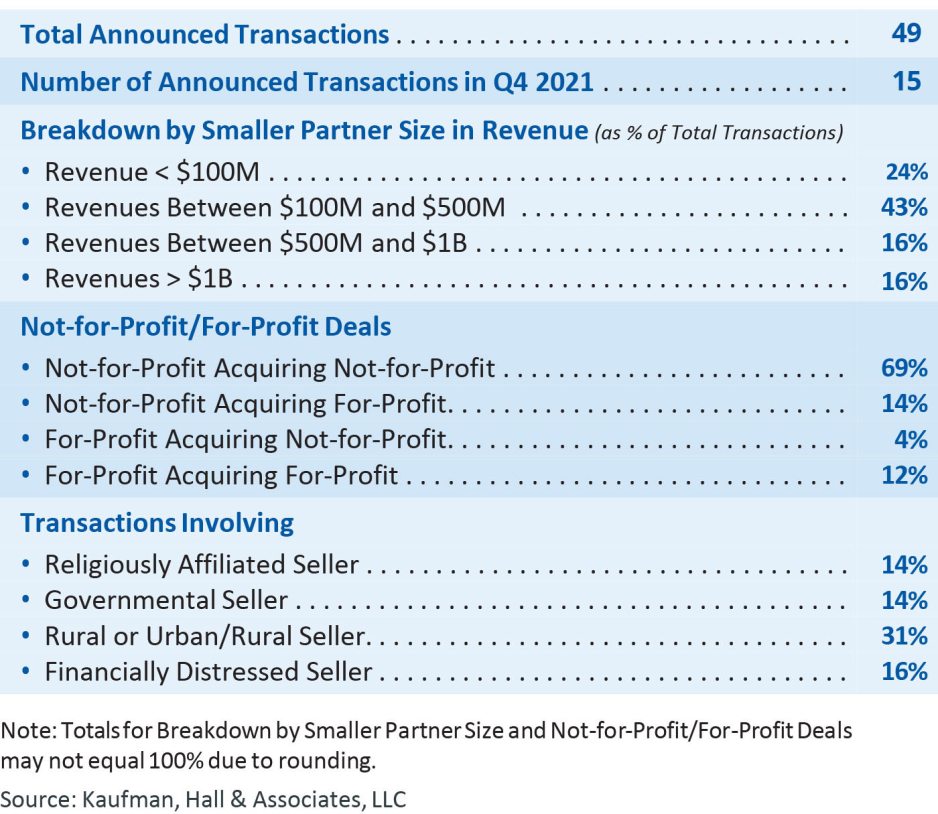

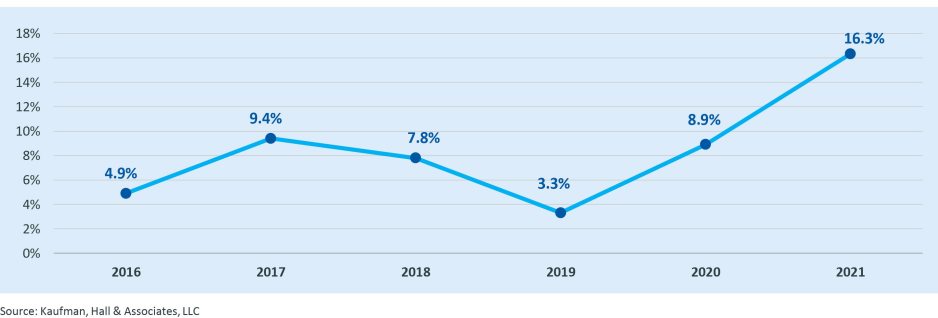

- The trend throughout 2021 was a smaller number of transactions being offset with a higher percentage of large transactions. Eight of the announced transactions in 2021 were “mega mergers” (transactions in which the seller or smaller partner by revenue had more than $1 billion in annual revenue). This year had the largest percentage of announced “mega merger” transactions in the last six years at 16.3%, almost double the percentage (8.9%) in 2020 (Figure 3).

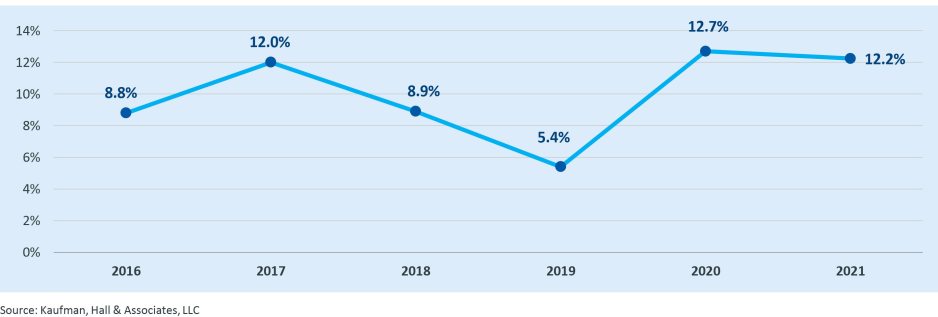

- Organizations with high credit quality were the smaller partner in a significant percentage of 2021 announced transactions, in line with 2020 levels and historical peaks. In more than one out of every 10 transactions, the smaller partner had a credit rating of A- or higher in 2021 (Figure 4).

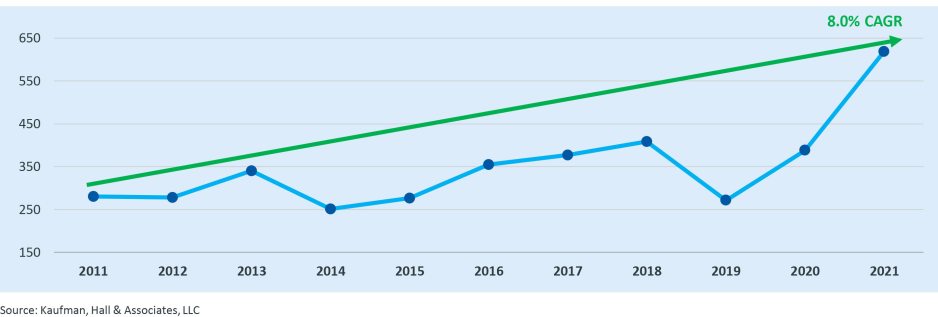

- As previously mentioned, the number of transactions in 2021 was down; however, the average size of smaller partner by annual revenue increased significantly to $619 million, up from $388 million in 2020. Since 2011, average smaller partner size by annual revenue has increased at a compound annual growth rate (CAGR) of approximately 8.0% (Figure 5).

- Activity by not-for-profit health systems as both acquirer and seller increased as a percentage of total transactions in 2021. Combined, transactions involving a not-for-profit partner represented 87% of announced transactions, compared with 81% in 2020.

- Transactions involving rural or urban/rural sellers increased to 31% of announced transactions from 24% in 2020. The number of financially distressed sellers remained flat at 16% of announced transactions from 2020 to 2021.

Figure 2: 2021 Hospital and Health System Transactions by the Numbers

Figure 3: Percentage of Announced Transactions in Which Seller’s (Smaller Party’s) Annual Revenue Exceeded $1B, 2016 – 2021

Figure 4: Percentage of Announced Transactions in Which Smaller Partner Had Credit Rating of A- or Higher, 2016 – 2021

Figure 5: Average Smaller Partner Size by Annual Revenue, 2011 – 2021 ($s in Millions)

Trends in 2021’s Most Significant Transactions

Announcements for the year’s ten largest transactions by revenue and several other notable transactions revealed the following trends.

Focusing on Core Assets and Markets

Some of 2021’s most significant transactions involved the sale of regional or market-concentrated facilities or assets in what appears to be a rebalancing of the core portfolio of multi-regional health systems. For example:

- In south Florida, Tenet Healthcare Corporation announced the sale of five hospitals and associated physician practices in Miami-Dade and southern Broward County to Steward Health Care for approximately $1.1 billion. The acquisition doubled the size of Steward’s presence in Florida, adding to the five hospitals it already operated in and around Melbourne and the Space Coast. The sale did not include Tenet’s ambulatory surgery centers in south Florida, which are separately operated by United Surgical Partners International.[i]

- In northern Georgia and Macon, HCA Healthcare sold four hospitals to Piedmont Healthcare for approximately $950 million, noting that the hospitals “were not able to fully benefit from a broader HCA presence in their areas.”[ii] At the same time, HCA continued to grow its presence in southeast Georgia, with the purchase of Meadows Regional Medical Center in Vidalia, Ga.

The divestiture and monetization of certain assets can free up resources to build deeper, more robust offerings in core service lines or markets. These pursuits may be in new markets or in other verticals, as these examples indicate.

Strengthening Intellectual Capital Resources

Academic medical centers sought to share and expand their expertise and enrich their intellectual capital in several new partnerships:

- East Carolina University’s (ECU’s) Brody School of Medicine and Vidant Health announced a joint operating agreement to create ECU Health, “with a goal of becoming a national academic model for providing rural healthcare.”[iii]

- The University of Oklahoma College of Medicine Faculty Practice and OU Health announced their plan to merge their hospitals and clinics into an integrated, comprehensive academic system that “fully unleashes the talent and collaboration across our faculty practice, clinics, and hospitals”[iv] and enhances Oklahoma’s ability to attract more intellectual talent to the state.

- King’s Daughters Health System and the University of Kentucky (UK) HealthCare announced a joint venture partnership to expand access to tertiary-level services for residents of eastern Kentucky and southern Ohio.

Clinical capabilities, expertise, and coordination were also a focus of the transaction involving University Health Care System in Augusta, Ga., and Piedmont Healthcare. University Health Care will become a regional hub for Piedmont, which will provide clinical expertise, services, and resources that allow Augusta-area residents to receive more care closer to home.

Capabilities in population health and value-based care featured in two of 2021’s largest transactions. Intermountain Healthcare announced its intention to “accelerate the evolution toward population health and value…across a broader geography”[v] through its merger with SCL Health, combining Intermountain’s successful model of value-based care—developed with its SelectHealth insurance division—with SCL’s expertise in successfully operating a multi-state system. And in Michigan, Spectrum Health announced its intention to merge with Beaumont Health, which will support expansion of Spectrum’s Priority Health Plan within southeast Michigan.

Addressing Societal Issues and Underserved Populations

The pandemic has focused new attention on issues of health equity and underserved populations, and addressing these issues is becoming a stated partnership goal.

- The creation of ECU Health, described above, is intended in part to facilitate new strategies and interventions for the most prevalent healthcare needs of the rural population that the newly formed system will serve. ECU’s Brody School of Medicine, one of the partners in the transaction, has an established focus on primary care in rural and other underserved areas, and ranks among the top 10% of medical schools nationally for graduating Black and Native American physicians.[vi]

- In the Chicago metropolitan area, the merger of Edward-Elmhurst Health and NorthShore University HealthSystem includes creation of a community investment fund—with each of the partners committing $100 million—to support partnerships with organizations working to enhance health equity and well-being and advance local economic growth.[vii]

- The merger between Intermountain Healthcare and SCL Health, also described above, is intended to serve as a model for combining the resources of faith-based and secular health systems in a merged organization that can “further extend its mission-focused approach to serving patients, particularly vulnerable populations.”

This trend is also evident in the growing number of partnerships between health systems and specialized behavioral, home health, and other non-acute providers, discussed in our Q3 2021 report, as health systems work to address the needs of populations affected by the social isolation and other adverse impacts of the pandemic.

Looking Forward: A New Phase in Healthcare Partnerships

Prior to the COVID-19 pandemic, the U.S. healthcare system had experienced two phases of partnerships:

- Phase One, which peaked in the 1980s and 1990s, saw independent hospitals combine into healthcare systems in an effort to contain rapidly rising healthcare costs and to respond to the new demands of managed care.

- Phase Two, which peaked in the 2010s (following passage of the Affordable Care Act), saw healthcare systems combine to attain or accelerate access to key resources to prepare for population health, tighter integration of healthcare services, and assumption of risk.

Even before the pandemic struck, new forces were laying the groundwork for a new phase of healthcare partnerships. Factors including the ongoing movement of care from inpatient to outpatient settings, technological change, and the push toward consumerism in healthcare created opportunities for legacy healthcare providers as well as new providers who could focus on a specialized segment of the market for healthcare services (e.g., primary care, behavioral health, ambulatory surgery, telehealth, home health, chronic care management, etc.) without bearing the high costs of providing acute inpatient services. As the Affordable Care Act’s encouragement of integration of services across the care continuum took hold, new industry participants were bringing focus and optimization in singular service lines, which is now opening up avenues to optimize various service providers in a single coordinated model.

With more participants and alternative sites and settings now available, consumers, health plans, and employers face an ever-growing assortment of choices for where they can receive (or pay for) care. Providers—both legacy and new—can differentiate themselves by being better, more affordable, or faster in the delivery of the services they choose to provide. Accordingly, health systems will increasingly be asking the rhetorical question of “what is our core business?” as they develop and execute strategic plans and initiatives.

The COVID-19 pandemic has further altered the healthcare landscape. Although hospitals and health systems had experienced financial disruptions—as recently as the Great Recession of 2008-09—they had never in recent history experienced disruption of their core operations as they have over the past two years. Disruptions in the supply chain and labor market have further pressured operating margins and may continue to do so over the long term. Societal impacts of the pandemic are producing heightened demand for high-touch specialty services in areas such as behavioral health and home health.

As healthcare organizations seek to stabilize their operations and move toward a new post-pandemic normal, their strategy will be influenced by three lessons of the pandemic:

- Realize the imperatives of scale. Larger systems were better positioned to deploy resources, segregate facilities for infected and non-infected patients, and weather the operational and financial impacts of the pandemic that hit different facilities and markets at different times.

- Focus on core markets and services. Operational disruptions and financial pressures made non-core assets or assets in non-core markets less attractive, prompting divestiture or monetization of these assets.

- Seek partnerships that add new capabilities or meet consumer demand for new or enhanced services. As discussed in our Q3 2021 report, health systems are seeking partnerships that can offer consumers access to new services or enhance the delivery of services that require specialized skillsets. These partnerships can enable health systems to focus on their core business and enhance or expand service offerings.

In many markets, hospitals and health systems are positioned to play a central role in navigating and managing a portfolio of offerings tailored to the needs and demands of their markets. They have an established brand, broad physician relationships, care coordination infrastructures (including EHRs), and the ability to care for co-morbidities that more specialized partners are not equipped to handle. We anticipate a greater willingness to engage with specialty providers to complement the traditional inpatient/outpatient services that have been the core offering of hospitals and health systems.

In the year ahead, we will continue to report on announced transactions between hospitals and health systems in our quarterly updates, and we will also look for opportunities to highlight transactions that illustrate this emerging new phase of healthcare partnerships.

Evaluating New Partnership Options

As hospitals and health systems consider new partnership models, key questions will include:

- What is our core business?

- For what services is there strong consumer need or demand?

- Are there potential partners who can provide these services better than we can?

- What do we offer to potential partners?

- What degree of control do we need or want in the partnership?

- What is the optimal structure for the partnership (e.g., ownership, branding, financial commitment, governance, clinical decision-making)?

Select 2021 Announced Transactions in Which Kaufman Hall Served as an Advisor

Hospital and Health System Transactions

- Carle Health/UnityPoint Health – Central Illinois

- Bryan Health/Kearney Regional Medical Center

- Piedmont Healthcare/University Health Care System

- King’s Daughters Health System/University of Kentucky HealthCare

Other Transactions

- Medica’s acquisition of a majority interest in Dean Health Plan, a subsidiary of SSM Health

- Altais’ acquisition of Family Care Specialists Medical Group, Inc.

- University of Miami Health System’s technical services agreement with Labcorp

- Labcorp’s acquisition of the outreach laboratory business of North Memorial Health

- UnitedHealthcare’s acquisition of PreferredOne from Fairview Health Services

- Fairview Health Services’ behavioral health joint venture with Acadia Healthcare

- Coastal Medical’s strategic partnership with Lifespan

*Bold text denotes the party for which Kaufman Hall served as advisor.

References

[i] Tenet Healthcare Corporation: “Steward Health Care to Acquire Five Hospitals in the Miami-Dade/Southern Broward Area from Tenet Healthcare.” Press release, June 16, 2021.

[ii] HCA Healthcare: “HCA Healthcare to Sell Four of Its Hospitals in Georgia to Piedmont Healthcare.” Press release, May 3, 2021.

[iii] Vidant Health: “ECU, Vidant Health Announce Joint Operating Agreement.” Press release, Nov. 12, 2021.

[iv] OU Health: “University of Oklahoma and Hospital Partner Announce Merger Intent to Create New Health System.” Blog post, March 9, 2021.

[v] SCL Health: “Intermountain and SCL Health Announce Intent to Merge.” Press release, Sept. 16, 2021.

[vi] Brody School of Medicine website: Meeting Our Mission: By the Numbershttps://medicine.ecu.edu/mission/

[vii] NorthShore University HealthSystem: “NorthShore and Edward-Elmhurst Health Announce Merger Plans.” Press release, Sept. 8, 2021.

Co-contributors:

Anu Singh, Managing Director and Leader of the Partnerships, Mergers & Acquisitions Practice, asingh@kaufmanhall.com

Kris Blohm, Managing Director, kblohm@kaufmanhall.com

Nora Kelly, Managing Director, nkelly@kaufmanhall.com

Courtney Midanek, Managing Director, cmidanek@kaufmanhall.com

Chris Peltola, Assistant Vice President, cpeltola@kaufmanhall.com

Blake Dorris, Senior Associate, bdorris@kaufmanhall.com

Matthew Santulli, Associate, msantulli@kaufmanhall.com

For media requests, please contact Haydn Bush at hbush@kaufmanhall.com.