"We have declared home health as the new frontier in value-based medicine.”

This quote by William Fleming, president of Humana Healthcare Services, was made in a March 2019 presentation to investors that followed upon Humana’s private equity-backed acquisition of Kindred at Home in 2018. In the same presentation, Humana— the nation’s second largest provider of Medicare Advantage plans—identified home health as one of the “five most impactful areas of influence in health.”1

There is a good deal of logic behind Humana’s focus on the home. The U.S. population is aging. Technology is expanding the range of medical services that can be delivered at home, as well as the ability to remotely monitor and connect with patients recovering from a procedure or managing a chronic condition. Home health is typically a much lower cost alternative to care delivered in institutional settings. Payers also are recognizing the value of home-based non-medical services that address social determinants of health and are revising or reinterpreting policies to allow payment for these services.

For health systems, a home-centered strategy that focuses on home health, non-medical home care, or both may be advantageous across a range of settings. Home health can help manage costs under value-based payment structures, including accountable care organizations (ACOs) and bundled payment models. Home care can increase patient satisfaction and help build consumer engagement with a health system through private-duty services that assist aging or recuperating individuals with the necessities of daily life. For those systems with providerbased health plans—particularly those offering Medicare Advantage plans—a home-centered strategy can help manage total cost of care, enhance member satisfaction, and offer a point of value differentiation in plan benefits.

Yet just as Humana staked its claim in the “new frontier” of the home through its acquisition of Kindred, health systems may find that a home-centered strategy is best pursued through a joint venture or partnership with an existing home health or home care operator. This article first takes a closer look at the case for home health and home care services as components of a home-centered strategy. It then discusses why a partnership option may be the best path to explore and provides some considerations for structuring a partnership.

Learn More About Partnership-Based Strategy

The Case for a Home-Centered Strategy

Home Health Services

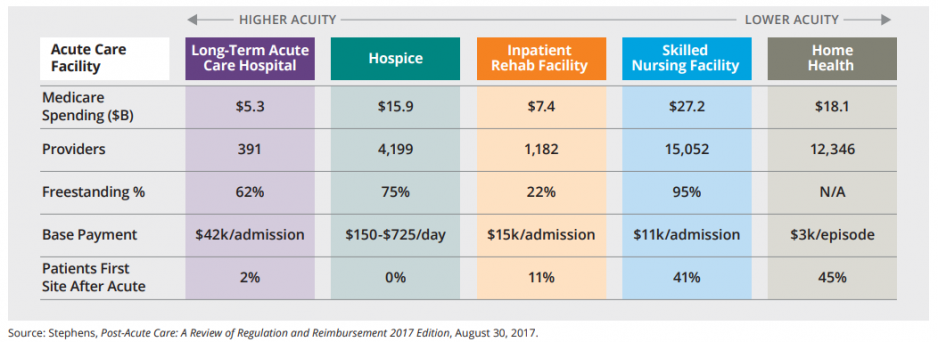

A comparison of home health with other areas of post-acute care highlights some of its advantages (Figure 1). It already is the leading site for post-acute care following an inpatient discharge. It is second only to skilled nursing facilities in Medicare fee-for-service spending, but costs for an episode of home-health care are significantly below the cost of an episode of care in a skilled nursing facility.

Home health’s position among post-acute care options is likely to strengthen, given projected growth trends, clinical outcomes evidence, and consumer preferences for at-home care. While there is some risk associated with changing payment models, home health operators have proven adept at containing cost growth.

Figure 1: Comparison of Post-Acute Sites of Care

Growth Trends

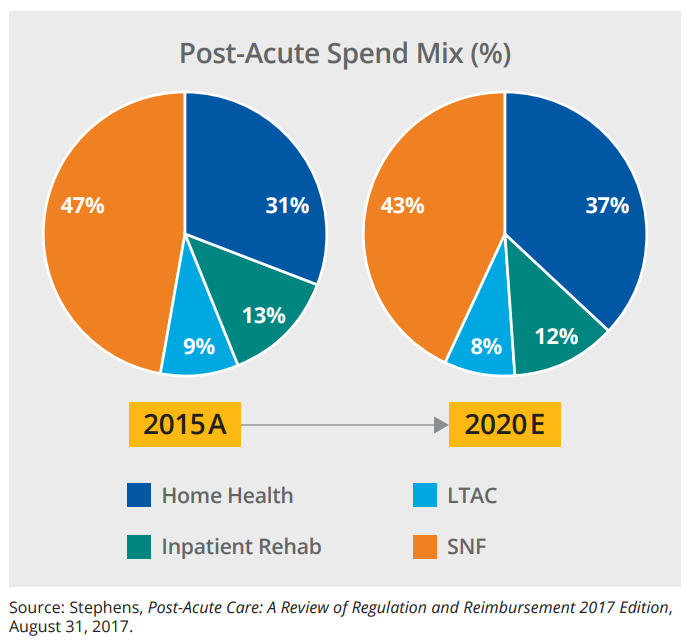

The CMS Office of the Actuary predicts that home health services will be one of the fastest growing areas of healthcare professional services over the next decade. National health expenditures for home health (defined as medical care provided by freestanding home health agencies, not including non-medical home care services) for Medicare beneficiaries (both fee-for-service and Medicare Advantage members) are projected to grow from just under $39 billion in 2018 to just over $81 billion in 2027. Although growth in total national home health expenditures lagged slightly behind growth in overall average national health expenditures from 2014 – 2016, it began to surpass the overall average in 2017 and is projected to exceed overall average growth in expenditures through 2027.2 Home health is also taking an increasing share of post-acute expenditures (Figure 2).

Figure 2. Growth in Home Health’s Share of Post-Acute Expenditures

Clinical Outcomes

Studies have found little difference in outcomes for patients who receive post-acute care at home instead of from a skilled nursing facility and have found the potential for significant cost savings. In a recent study using Medicare data for more than 17 million hospitalizations, researchers found no significant differences in non-discretionary readmissions, functional status, or mortality rates between patients discharged to home compared to those discharged to a skilled nursing facility. Medicare payments for post-acute care for patients discharged to home were more than $5,000 lower than payments for those discharged to a skilled nursing facility.3

Similarly, studies of bundled payment programs, such as CMS’s Bundled Payments for Care Improvement (BPCI) initiative, have shown that provider organizations that have successfully reduced costs generated the largest savings in post-acute care, particularly by reducing utilization of skilled nursing facilities and inpatient rehabilitation facilities and leveraging home care supports. Changes in post-acute-care utilization have not affected patient outcomes.4

Consumer Preferences

While there have not been significant studies of consumer preferences for home health over institutional post-acute care, there is clear data that consumers would prefer to stay in their home as long as possible and avoid hospitalization and intensive care in the later stages of life.5 Studies also indicate that patients who receive home health rate their experience more highly than patients who receive care in an institutional setting.6

Payment Trends

As of January 1, 2020, the Home Health Patient-Driven Group Model will go into effect for home health services for traditional Medicare beneficiaries. As required by the Bipartisan Budget Act of 2018, the time for an initial episode of home health care will be halved from 60 to 30 days (although an initial certification will cover the first two 30-day episodes of care) and payment will no longer be determined by the number of therapy visits. Instead, payment for an episode of home health care will be based on five factors, including whether the episode is early or late in the treatment plan, and whether it follows an institutional discharge or community referral. The patient’s clinical grouping (based on primary diagnosis), level of functional impairment, and comorbidity adjustment make up the remaining three factors. The changes are intended to be budget-neutral and financial impacts on the home health sector are not yet known.7

Anticipated growth in home health spending in the Medicare program may also be offset by budget considerations that will likely put downward pressure on payment rates, especially in the traditional Medicare fee-for-service program. The Medicare Payment Advisory Commission (MedPAC) is already recommending a 5 percent reduction in the Medicare base payment rate for home health agencies (HHAs) because the home health industry has successfully maintained Medicare margins in excess of 15 percent. MedPAC attributes these margins in part to HHAs’ ability to keep cost increases below 1 percent in many recent years.8

The possibility of reduced rates for home health should be weighed against the savings that a home health strategy could generate under risk-based payment structures. For health systems that have substantial exposure to risk-based payments or anticipate greater exposure in the future, or have a providersponsored Medicare Advantage plan, a home health strategy may be an important component in the effort to reduce costs without compromising clinical outcomes. Another consideration offsetting the risk of reduced rates is the proven ability of HHAs to control costs, which adds to their value as a partner in a health system’s home-centered strategy.

Home Care Services

A combination of demographic and policy trends makes a home-centered strategy that incorporates personal home care services worth consideration. These trends include growth in the senior population, an impending shortage of family caregivers, the interest of new market entrants, and a new focus on social determinants of health, including changes in Medicare Advantage plan regulations that now allow plans to offer supplemental benefits addressing social determinants of health.

Growth Trends

With substantial growth in the population aged 65 and older, and the expressed desire by individuals in this population group to remain in their home as long as possible, the opportunities for personal home care services will grow significantly. The U.S. Census Bureau predicts that the over-65 age group will grow from 49.2 million in 2016 to 78 million in 2035.9

A recent study draws attention to an important segment of the senior population: middle-income seniors who are too wealthy to qualify for public means-tested programs, but who do not have sufficient resources to afford the costs of senior housing communities for a sustained period of time.10 Middle-income seniors ages 75 – 84 will increase from 5.57 million in 2014 to 10.81 million in 2029, and will create a significant market for personal care services that assist in their daily living needs and provide a more affordable option to senior housing.

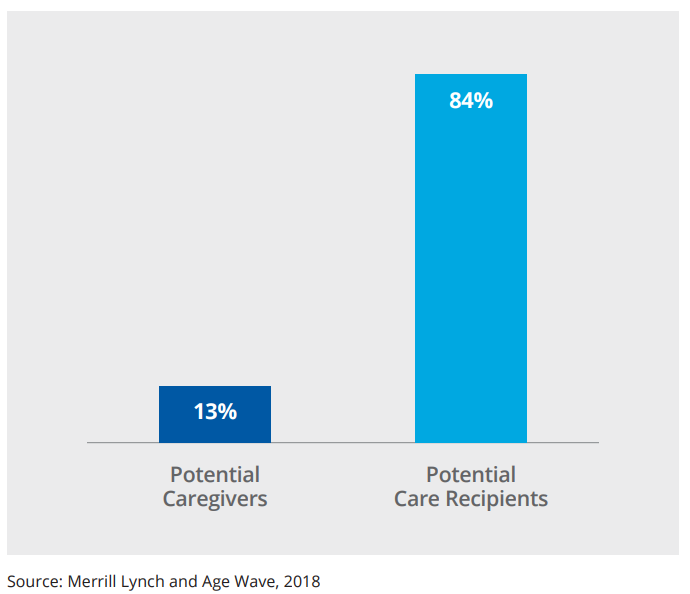

Growth in the senior population will also put strains on the ability of family members to serve as caregivers. The number of potential care recipients is estimated to grow by 84 percent from 2015 to 2050; over the same period, the number of potential caregivers is estimated to grow by only 13 percent (Figure 3).11 This likely will intensify the need to supplement or replace the estimated $500 billion in free care provided by family caregivers annually with paid services.12

Figure 3: Growth in Number of Care Recipients from 2015 to 2050 Outpaces Growth in Number of Caregivers

New Market Entrants

Home care is attracting interest from new sectors. Best Buy, the electronics retail giant, has spent the past two years investing in remote-monitoring equipment, senior-focused tech devices (including smart phones and medical alert devices), and other technologies designed to help seniors keep living in their home. Best Buy also owns the Geek Squad, comprised of approximately 20,000 employees who could serve as consultants to home-based seniors. A recent report from Morgan Stanley notes, “We don’t think the market fully grasps Best Buy’s commitment to health. We believe Best Buy has a durable competitive advantage in senior care, its niche in the healthcare services market.”13

Best Buy’s interest draws upon its extensive consumer capabilities and suggests how health systems could build their own consumer capabilities in areas outside of traditional private-duty services to engage with the growing senior market. It also suggests that the range of potential partners for home care services might extend beyond traditional home care and home health operators. The Morgan Stanley report notes Best Buy’s potential to target providers with Medicare Advantage plans in shared savings partnerships, a potential that has been strengthened by policy changes in the Medicare Advantage program.

Policy Changes

An important policy change for personal home care services is now in effect for the growing segment of Medicare Advantage plans, which have seen enrollment nearly double over the past decade.14 In 2018, CMS reinterpreted the definition of allowable supplemental benefits offered by Medicare Advantage plans to include services that might have been considered daily maintenance, and thus not allowable under the previous interpretation, but address social determinants of health. These services might include adult day health services or in-home support services or devices. Plans were able to begin offering new supplemental benefits in 2019.15 At the same time, CMS reinterpreted the uniformity requirement for Medicare Advantage plans, allowing access to supplemental benefits tied to specific disease states, as long as similarly situated individuals are treated uniformly. This could allow plans to offer services such as carpet shampooing for patients with asthma, or transportation to grocery stores for patients with diabetes. These changes will provide Medicare Advantage plans much more flexibility to pay for personal home care services that help plan members avoid higher cost hospitalizations, readmissions, or emergency care utilization.

Understanding Social Determinants of Health

Despite widespread belief that addressing social determinants of health can have significant beneficial impacts, there is still limited evidence of which interventions are most effective, and for which populations. A home-centered strategy that focuses initially on private-pay home care services can start to build that understanding, while positioning the health system to serve the daily needs of a growing senior population.

Health systems with provider-sponsored Medicare Advantage plans might also consider partnering with home care operators or other organizations that have developed experience in addressing social determinants of health. A study of Medicare Advantage plans that are considering new supplemental benefits indicates than plans are interested in such partnerships, especially when the partner has proof of the efficacy of an intervention, is willing to take on some degree of risk, and has the capability to scale the intervention across the plan’s membership.16

Examples of Home-Centered Strategies

Recent examples of home-centered strategies that incorporate home health or home care components include the following:

- Home health. Health systems that have a significant number of attributed lives in an ACO, extensive involvement in bundled payment models, or a provider-sponsored health plan that offers Medicare Advantage or Medicaid managed care plans can see significant results from a home health strategy that targets post-acute care for patients following an inpatient discharge. An example is the joint venture between Summa Health in Ohio and home health and hospice services provider Alternate Solutions Health Network. Although Summa Health had a profitable home health and hospice business, it needed new capabilities and greater scale to serve the needs of covered lives in its ACO and provider-sponsored Medicare Advantage plan.

- Home care. Several health systems have begun to expand their ability to offer private-pay services to older consumers seeking to remain independent and in their home. An example is the Homespire joint venture between Intermountain Health and Lifesprk, which offers private-pay services to seniors in Intermountain markets throughout Utah.

The Summa Health and Intermountain examples both rely on joint ventures with home health and home care operators, and they are not unique. Although demand for home-centered services is likely to grow, many health systems have been divesting their home-centered operations and are opting for joint ventures or other partnerships with home health and home care operators instead.

The Partnership Option

A home-centered strategy based on a joint venture or other form of partnership with a home health or home care operator often will offer the best path forward for a health system. While home-centered care represents a growth opportunity, it also represents a small percentage of revenue for most health systems and may not receive the same attention as higher-stake business areas. Home health and home care operators have a very different cost structure than traditional health systems, with minimal facility needs and lower pay scales for clinical staff, home health aides, and caregivers. They currently face a labor shortage and the prospect of upward pressure on wages, but they have also proved more adept than large health systems at managing costs, in part because of their leaner cost structure. Home health and home care operators, which historically have been fragmented and small, also bring new levels of sophistication to a partnership as mergers and acquisitions have built companies with regional and even national scale.

Partnership offers health systems several benefits:

- Creating a partnership that leverages the resources of an existing home health or home care operator can provide a faster route to bringing a home-centered program up to scale.

- A home health or home care operator already will have the bandwidth and skills to manage a home-centered program. They may also have expertise in areas such as improved patient experience and data analytics to inform post-acute care decisions.

- Home health and home care operators have experience with the employee recruitment and compensation issues unique to the business, including relatively high employee turnover.

- A partner operator can free up health system management expertise and capacity to address other strategic priorities.

There are some key considerations for health systems when structuring a partnership. First, the health system should enter into the partnership with a clear view of what it hopes to achieve. It should work with its potential home health or home care partner to define mutually agreed upon financial and quality of care metrics for the partnership and milestones for determining the partnership’s success.

Next, if a health system is trying to build a home-centered strategy, it will not want to make the success of that strategy dependent solely upon its partner’s performance. The health system should negotiate appropriate control provisions to ensure that its community mission is enhanced and that incentives are aligned to support broader strategic objectives such as population health management. It should also define an exit strategy if the partnership does not meet expectations. This can be structured in different ways. For example, the health system might have the right to buy out its partner’s interest at a predetermined milestone if the partnership has not produced the intended results. Alternatively, the agreement might specify that breach in performance of agreed-upon quality or financial metrics can trigger the health system’s option to buy out its partner’s interest and terminate the partnership agreement.

A home-centered strategy aligns both with a health system’s interest in engaging with and meeting the needs of an aging population and with the increasing demand for high-quality, low-cost care delivery models. Home health and home care operators already know the terrain of this new frontier. For health systems seeking to stake a claim in home health, home health and home care operators can be valuable partners in executing a successful home-centered strategy.

References

1 Humana: “Investor Day 2019.” PowerPoint presentation. March 19, 2019.

2 Centers for Medicare & Medicaid Services, Office of the Actuary: National Health Expenditure Projections, 2018 – 2027. Feb. 26, 2019.

3 Werner, R., Coe, N., Qi, M., Konetzka, T.: “Patient Outcomes After Hospital Discharge to Home with Home Health Care vs to a Skilled Nursing Facility.” JAMA Internal Medicine, vol. 179(5), 2019. While the study did find a higher rate of discretionary readmissions for patients discharged to home, this was offset by a significantly lower Medicare payment for initial post-acute care and for a total 60-day episode of care, including hospitalization, all post-acute care, and subsequent readmissions.

4 Glickman, A., Dinh, C., Navathe, A.: “Issue Brief: The Current State of Evidence on Bundled Payments.” University of Pennsylvania, Leonard Davis Institute of Health Economics, vol. 22, no. 3. Oct. 8, 2018.

5 Landers, S., et al.: “The Future of Home Health Care: A Strategic Framework for Optimizing Value.” Home Health Care Management & Practice, vol. 28(4), 2016.

6 Federman, A., Soones, T., DeCherrie, L., Leff, B., Siu, A.: “Association of a Bundled Hospital-at-Home and 30-Day Postacute Transitional Care Program with Clinical Outcomes and Patient Experiences.” JAMA Internal Medicine, vol. 178(8). August 2018.

7 McCann, C.: “The New Home Health Reimbursement Rule Is Not the End of the Road.” HomeCare, Jan. 2, 2019.

8 Medicare Payment Advisory Commission: Report to the Congress: Medicare Payment Policy. March 2019.

9 U.S. Census Bureau: An Aging Nation: Projected Number of Children and Older Adults. March 13, 2018.

10 Patterson, C., et al.: “The Forgotten Middle: Many Middle-Income Seniors Will Have Insufficient Resources for Housing and Health Care.” Health Affairs. April 24, 2019.

11 Merrill Lynch and Age Wave: The Journey of Caregiving: Honor, Responsibility and Financial Complexity. 2018.

12 Ansberry, C.: “America Is Running Out of Family Caregivers, Just When It Needs Them Most.” Wall Street Journal. July 20, 2018.

13 Sudo, C.: “Why Best Buy Could Disrupt Senior Care More Than Rivals Like Amazon,” Senior Housing News, Sept. 26, 2019.

14 Jacobson, G., Damico, A., Neuman, T.: “A Dozen Facts About Medicare Advantage.” Kaiser Family Foundation, Nov. 13, 2018.

15 Holly, R.: “The Top Trends in Home Care for 2019.” Home Health Care News. Jan. 6, 2019.

16 Thomas, K., et al.: “Perspectives of Medicare Advantage Plan Representatives on Addressing Social Determinants of Health in Response to the CHRONIC Care Act.” JAMA Network Open, vol. 2(7), July 12, 2019.