2020 was off to a strong start in hospital merger and acquisition activity, with the number of announced transactions in Q1 among the highest seen in the past four years. Then the COVID-19 pandemic struck with full force in March. Unlike past shocks the healthcare industry has sustained, which typically have been related to changes in regulation or reimbursement, the pandemic was a direct hit on the delivery of acute care. Many health systems experienced both a liquidity crunch, as revenue flows dried up in the wake of canceled procedures, and an ongoing grind of diminished volumes, heightened labor and supply expenses, and continued surges of the virus that placed extraordinary demands on both frontline staff and management. Aside from the economic shock, the focus of many management teams on clinical and operational needs affected their ability to focus on certain long-term strategic initiatives, including partnership activity.

In the face of these pressures, it is remarkable that M&A activity for the year stayed within the historic range of activity seen over the past 10 years (Figure 1). As noted in our quarterly activity report for Q3, it appears that COVID-19 has actually confirmed the strategic rationale underlying many transactions that were already underway, and may be acting as a catalyst for innovative strategic partnerships and tactical transactions. The pandemic has accelerated the need for strategic initiatives that address the opportunities of industry transformation and that reward well thought-out alignment opportunities.

Figure 1: Number of Announced Transactions, 2010–2020

Source: Kaufman, Hall & Associates, LLC

This report includes a “Year in Numbers” summary of activity between hospitals and health systems and discusses key trends that emerged over 2020 and that we anticipate to see in 2021, as the COVID-19 pandemic has compelled healthcare organizations to:

- Focus on core business strengths and assess the long-term viability of non-core assets, aligning as needed with partners that offer complementary, innovative, or otherwise unrepresented capabilities

- Build partnerships to address gaps in the healthcare infrastructure exposed or intensified by the virus, including collaborative partnerships with non-traditional partners

- Strengthen intellectual capital resources to be nimbler and more flexible in dealing with the current crisis and in pivoting to new modes of providing care more efficiently, effectively, or uniquely relative to other legacy providers and potential new market entrants

The Year in Numbers

Trends in the data for 2020 include the following:

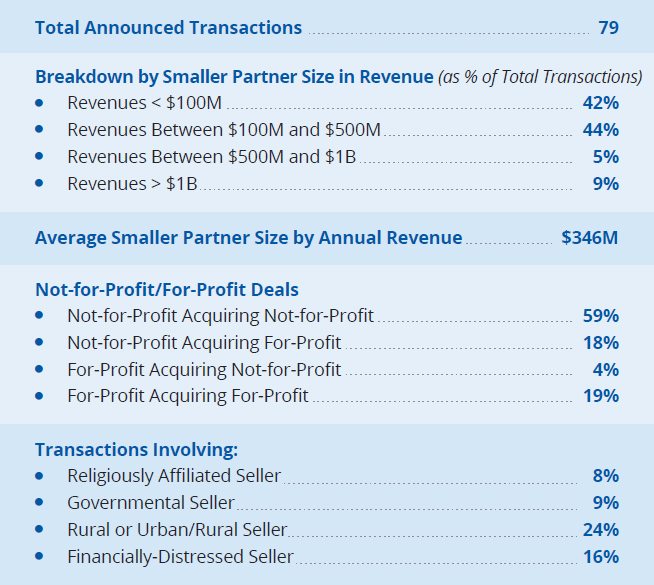

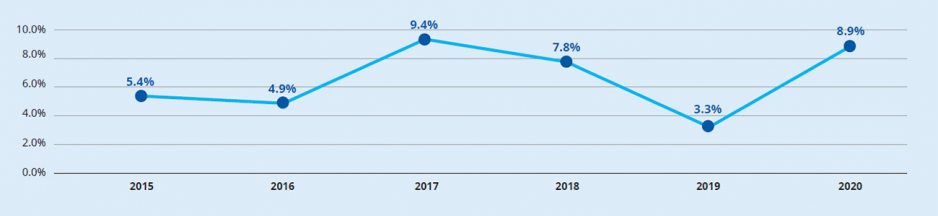

- Organizations with significant scale and high credit quality were the smaller partner in a significant percentage of 2020 announced transactions, in line with historical peaks. Seven of the announced transactions in 2020 were “mega mergers” (transactions in which the seller or smaller partner by revenue had more than $1 billion in annual revenue), up from three such transactions in 2019 (Figure 3).1 In 10 transactions, the smaller partner had a credit rating of A- or higher in 2020, up from five such transactions in 2019 (Figure 4).

- In line with growth in the number of mega mergers announced in 2020, the average size of smaller partner by annual revenue increased to $346 million, up from $278 million in 2019. Since 2010, average smaller partner size by annual revenue has increased at a compound annual growth rate (CAGR) of 6.2% (Figure 5).

- Activity by for-profit health systems as both acquirer and seller increased as a percentage of total transactions in 2020. Combined, transactions involving a for-profit partner represented 37% of announced transactions, compared with 23% in 2019, with a nearly even split between transactions in which the for-profit partner was acquirer versus seller.

- Although the impacts of the COVID-19 pandemic resulted in a lower number of announced transactions (79 in 2020 compared to 92 in 2019), the number of announced transactions remained within the historical range of the past 10 years, as shown in Figure 1.

- The number of financially distressed sellers was stable but lower in 2020, down to 16% of announced transactions from 20% in 2019.

Figure 2: 2020 Hospital and Health System Transactions by the Numbers

Source: Kaufman, Hall & Associates, LLC

Figure 3: Percentage of Announced Transactions in Which Smaller Partner's Average Annual Revenues Exceeded $1 Billion, 2015–2020

Source: Kaufman, Hall & Associates, LLC

Figure 4: Percentage of Announced Transactions in Which Smaller Partner Had Credit Rating of A- or Higher, 2015–2020

Source: Kaufman, Hall & Associates, LLC

Figure 5: Average Smaller Partner Size by Annual Revenue, 2010–2020

Source: Kaufman, Hall & Associates, LLC

Focusing on Core Business Strengths

Kaufman Hall believes that a key differentiator among hospitals and health systems in the coming years will be their ability to build resiliency in the face of both industry disruption and unexpected market shifts. This will require both the full and strategic deployment of all resources the organization has available, and a relentless and continuous focus on performance improvement. Health systems encountered the COVID-19 crisis with varying levels of balance sheet resources and varying levels of operating strength across markets, as shown in the at-risk-to-thriving grid in Figure 6. Health systems that entered the crisis with strong balance sheet resources and that have been able to avoid or minimize damage to their operations will be in a position to take advantage of new opportunities presented by other systems’ divestitures, growing their capabilities and expanding their core strengths into new markets. They also will be sought as partners by potential market disruptors or innovators or will reposition their own ability to innovate and thrive in new paradigms of how care will be delivered, financed, and otherwise optimized.

Figure 6: Health System Resiliency

Source: Kaufman, Hall & Associates, LLC

An emphasis on resiliency will bring a greater focus to what “core” business activities will drive the future direction of hospitals and health systems. Organizational leaders will have to look hard at underperforming service lines and facilities to determine how and how much they contribute to the overall enterprise.

For-profit health systems are making these assessments and, where appropriate, have divested or created partnerships to manage underperforming operations and non-core assets. We commented on this trend within the acute space in our quarterly activity report for Q2, in which six of the 14 announced transactions represented divestitures by major for-profit health systems. We expect that for-profit health systems will continue on this path and, along with larger not-for-profit systems, will refocus on core businesses and markets in an effort to build resiliency. On the not-for-profit side, 2020 announced transactions representative of this trend include VCU Health System’s acquisition of hospital and physician practices in the Northern Neck and upper Middle Peninsula region of Virginia from Riverside Health System and Carle Health System’s acquisition of two hospitals in central Illinois from Advocate Aurora Health.

Building Partnerships to Address Infrastructure Gaps

The COVID-19 pandemic has exposed critical gaps in the healthcare infrastructure, while underscoring the advantages of regionalization and scale in meeting the public health needs caused by the crisis.

Many hospitals and health systems have struggled operationally and financially as the coronavirus has surged and resurged across the country. But challenges have been most acute at smaller, independent hospitals that do not have the resources of larger, well-organized systems. An October 2020 Health Affairs blog noted that hospitals with fewer than 50 ICU beds have had higher COVID mortality rates, while there have been significantly fewer fatalities from Acute Respiratory Distress Syndrome (ARDS)—a common condition in severely ill COVID patients— at high-volume hospitals with staff that are more experienced in treating ARDS patients. These disparities have demonstrated the “long identified survival benefits of regionalization, whereby ARDS patients could be transferred to well-equipped hospitals that perform a high annual volume of mechanical ventilation.”2 Regionalization also minimizes the conflicting incentives of the existing, fragmented healthcare system, in which independent hospitals may be reluctant to transfer patients to larger hospitals because of concerns related to revenue losses.

A separate article by Health Affairs’ Council on Health Care Spending and Value reiterates the significance of regionalization in improving the value of services for which higher volume is associated with better quality, and also notes that consolidation “can result in the preservation of access to care, such as in rural areas, where hospital consolidation may be the only alternative to closure.”3 This is a compelling issue for financially stressed, urban safety-net hospitals as well, but 2020 revealed how difficult efforts to preserve access through consolidation can be. For example:

- A planned merger of four safety-net hospitals in south Chicago, announced in January 2020, stalled when the Illinois state legislature failed to approve funds necessary for the merger to go forward.4

- In February 2020, the Federal Trade Commission announced its intent to challenge the planned merger between Jefferson Health and Einstein Healthcare Network, which would preserve access to care in some of Philadelphia’s poorest neighborhoods. Court rulings favorable to Jefferson and Einstein mean the merger might be able to occur in 2021, but with the addition of millions of dollars in legal fees necessary to defend the merger.5

Strengthening Intellectual Capital Resources

Hospitals and health systems have been tasked with rapid implementation of telehealth services, development and dissemination of new clinical protocols, rebuilding of supply chains, management of vaccine trials, and a host of other, unexpected innovations and adaptations as they respond to the pandemic. Health systems with significant depth of intellectual capital and expertise have had an upper hand in addressing these challenges.

The importance of strengthening access to intellectual capital resources was reflected in announced transactions in which strong, independent community and regional health systems joined with larger systems with academic medical centers and teaching hospitals. Several of these transactions were initiated pre-pandemic; again, the pandemic only strengthened the rationale for pursuing them. These include:

- New Hanover Regional Medical Center’s decision to join Novant Health in a partnership with the UNC School of Medicine in North Carolina

- Northwest Community Healthcare’s plan to merge with NorthShore University Health System in Illinois

- Saint Peter’s Healthcare System’s signing of a definitive agreement to merge with Robert Wood Johnson Barnabas Health in New Jersey

- Lake Health’s decision to join University Hospitals in Ohio

Several large-scale transactions announced in 2020 would bring together health systems from different geographies and allow the partners to gain access to different capabilities or continue to strengthen value-based care models. One such example was the Cone Health (North Carolina) and Sentara Healthcare (Virginia) transaction. “This rapidly changing healthcare environment requires tremendous transformation and innovation to ensure the long-term success of each respective health system and, most importantly, the very best for those we are privileged to serve,” said Howard P. Kern, president and CEO of Sentara Healthcare. “We can either react to change, or we can shape it. We are choosing to shape change and will lead this transformation of healthcare together.”6

As health systems face ongoing uncertainty and work to transform healthcare, intellectual capital will be as important as scale in helping them respond nimbly and efficiently to new challenges.

Looking Forward

2021 promises to be a transformative year in healthcare. With COVID-19 vaccines now being administered around the country, a potential end to the pandemic is in sight. But the lessons of the pandemic will be a catalyst in reshaping the U.S. healthcare system for years to come. We anticipate the following:

- New strategic imperatives. The pandemic may result in permanent changes to the healthcare business model. Demand for telehealth likely will remain above pre-pandemic utilization levels as consumers recognize the convenience of digital services; health systems will need to adapt to a new balance between virtual and in-person visits. Volumes for many services fell significantly during the pandemic; they may be slow in recovering to pre-pandemic levels.

- An emphasis on addressing broader societal issues. A new focus on addressing disparities in healthcare outcomes—one of the priorities of the incoming Biden administration—may put a new emphasis on social determinants of health and treatment of chronic conditions. Reducing the need for care in the first place is a critical element in addressing disparities in outcomes. It is our expectation that the largest and broadest health systems will be most capable and influential in engaging in socially driven programs that reduce the overall cost and intensity of “sick” care, as efforts to maintain wellness among underprivileged populations accelerate.

- A growing diversity of partners and partnerships. While this report focuses on M&A activity between hospitals and health systems, we also anticipate significant growth in partnerships among and between other healthcare verticals. Even as health systems divest non-core assets in areas such as skilled nursing, home health, behavioral health, laboratories, and post-acute care, these divested assets may be replaced by partnerships with specialty service providers to ensure health system consumers maintain access to a full continuum of services. Limitations on fee-for-service payment structures exposed by the pandemic may increase the number of payer-provider partnerships around new payment and care delivery models. Physician groups hit hard by the pandemic’s financial impacts also will be seeking new partnerships that provide greater financial security. Rapid development of digital healthcare models will spur new partnerships as well.

This report was published on January 7, 2021

Read through other M&A Reports

References

1 The seven announced “mega merger” transactions do not include the announced transaction between Intermountain Healthcare and Sanford Health. Because this transaction was both announced and cancelled in the same quarter of 2020, it did not meet our criteria for recognition of announced transactions, which we calculate on a quarterly basis.

2 Pollack, H., and Kelly, C.: “COVID-19 and Health Disparities: Insights from Key Informant Interviews.” Health Affairs, Oct. 27, 2020. https://www.healthaffairs.org/do/10.1377/hblog20201023.55778/full/

3 Tollen, L, and Keating, E.: “COVID-19, Market Consolidation, and Price Growth.” Health Affairs, Aug. 3, 2020. https://www.healthaffairs.org/do/10.1377/hblog20200728.592180/full/

4 Goldberg, S.: “Government Funding to Fuel Chicago Hospital Merger Falls Through.” Modern Healthcare, May 24, 2020. https://www.modernhealthcare.com/finance/government-fundingfuel-chicago-hospital-merger-falls-through

5 Brubaker, H.: “FTC Seeks to Stop Jefferson’s Acquisition of Einstein Healthcare by Appealing Judge’s Decision.” The Philadelphia Inquirer, Dec. 9, 2020. https://www.inquirer.com/business/health/jefferson-ftceinstein-philadelphia-merger-hospitals-ibc-anti-trust-20201209.html

6 Sentara Healthcare: “Sentara Healthcare, Cone Health Join Forces to Transform Healthcare.” Press release, Aug. 12, 2020. https://www.sentara.com/aboutus/news/news-articles/sentara-healthcare-conehealth-join-forces-to-transform-healthcare.aspx