Hospitals and health systems across the country continued to see gains in April compared to devastating losses in the early months of the COVID-19 pandemic. Margins, volumes, and revenues increased across most performance metrics both year-to-date (YTD) and year-over-year (YOY), but were down compared to March 2021. Total expenses, however, continued to increase both YTD and YOY, but saw moderate decreases month-over-month (MOM).

National COVID-19 metrics declined the latter part of the month after rising steadily in late March and early April, according to Centers for Disease Control and Prevention data.1 The 7-day moving average of new COVID-19 cases fell 27% from a monthly high of 69,097 on April 13 to 50,108 on April 30. The 7-day moving average of new admissions for patients with confirmed COVID-19 fell from a monthly peak of 5,774 on April 18 to 4,975 on April 30. The declines came even as the pace of vaccinations continued to slow, with the 7-day moving average of daily doses administered falling from a peak of 3.3 million per day in mid-April to 2.3 million on April 30. By month’s end, 107 million Americans had been fully vaccinated.

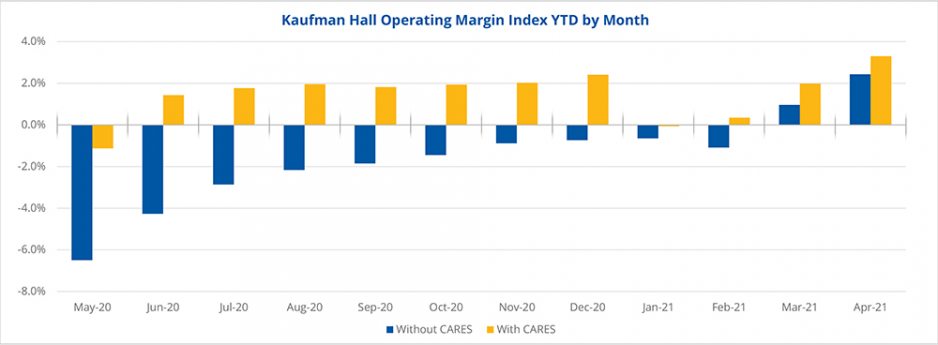

Hospital margins remained relatively thin. Not including federal CARES funding, the median Kaufman Hall hospital Operating Margin Index2 was 2.4% in April. With the funding, it was 3.3%. The median Operating EBITDA Margin was 7.1% without CARES and 8.1% with CARES.

YTD and YOY margin results were especially high for a second month in a row, as Kaufman Hall’s analyses compare April performance to the first full month of the pandemic in April 2020. In April 2021, Operating Margin rose 101.9% YTD or 8.6 percentage points, and Operating EBITDA Margin rose 102.2% or 8.1 percentage points, not including federal CARES funding. With the funding, Operating Margin was up 90.6% YTD or 6.9 percentage points and Operating EBITDA Margin increased 77.7% or 6.2 percentage points. Compared to April 2020, Operating Margin was up 113.1% (39.3 percentage points) without CARES and 109.5% (21.4 percentage points) with CARES, while Operating EBITDA Margin rose 129.7% (36 percentage points) without CARES and 117.8% (19.4 percentage points) with CARES.

It is important to keep April’s margin gains in context. Rather than significant strength in overall hospital performance, they reflect a contrast to the brutal losses experienced at the start of the pandemic. In April 2020, nationwide shutdowns and severe restrictions on outpatient procedures caused Operating Margins to plummet 282% (30.3 percentage points) YOY and Operating EBITDA Margins to fall 174% (27.9 percentage points) YOY.

In April 2021, hospitals nationwide saw volumes increase across most metrics YTD and YOY, but decrease slightly compared to March. Adjusted Discharges were up 5.9% YTD and jumped 66.4% YOY, while Adjusted Patient Days rose 10% YTD and 64.8% YOY. Both metrics fell 1.0% MOM.

Emergency Department (ED) Visits were mixed, falling 7% compared to the first four months of 2020 but rising 57.2% YOY and 5.3% MOM. Operating Room Minutes were down 3.6% MOM, but increased 26.1% YTD and shot up 189.2% YOY compared to April 2020, when initial COVID-19 restrictions abruptly halted most outpatient procedures.

Revenues followed a similar pattern, with Gross Operating Revenue (not including CARES) up 16.7% YTD and 71.8% YOY, but down 2.5% compared to prior month. Inpatient Revenue rose 10.6% YTD and 37.1% YOY, but was down 1.9% MOM. Outpatient Revenue rose 20.3% YTD and jumped 114.8% compared to April 2020, but fell 2.0% from March.

U.S. hospitals and health systems continued to see total expenses rise compared to 2020 levels. Total Expense was up 6.6% YTD and 13.1% YOY, Total Labor Expense increased 6.1% YTD and 9.4% YOY, and Total Non-Labor Expense rose 7.0% YTD and 16.3% YOY. Compared to March, however, all three metrics were down about 3%.

Expense results were more mixed when adjusted for the month’s volumes. Total Expense per Adjusted Discharge increased 2% YTD, but fell 32.3% YOY and 2% MOM. Labor Expense per Adjusted Discharge was flat YTD, and declined 34.3% YOY and 2.6% MOM. Non-Labor Expense per Adjusted Discharge increased 2.8% YTD, but was down 31.5% YOY and 1.7% MOM.

The U.S. economy saw hiring fall short of expectations in April, with nonfarm payrolls increasing by only 266,000 and March’s figure revised down by 146,000 jobs from 916,000. Meanwhile, inflation sped up in April as the Consumer Price Index rose 4.2% from the prior year—its sharpest increase since September 2008. Commodity prices continue to rise, with lumber up 124% in 2021 and copper up 36%. Federal Reserve officials reiterated their stance of not raising interest rates or reducing monthly bond purchases unless inflation remains elevated over an extended period.

U.S. hospitals and health systems likely will see continued margin, volume, and revenue gains in the coming months compared to dramatic losses seen in the early months of COVID-19. Fluctuations MOM, however, illustrate the continued uncertainties perpetuated by the pandemic. Numerous factors will influence the pace of recovery, including the trajectory of vaccination efforts and the continued spread of COVID-19 variants. Healthcare leaders must remain vigilant in efforts to monitor and improve performance as they move forward through this second year of an ongoing pandemic—the end of which remains yet to be determined.