Key Observations

U.S. hospitals and health systems saw mixed performance in March as national COVID-19 metrics plateaued early in the month before climbing steadily again with increased spread of COVID-19 variants, rising travel rates, and further lifting of pandemic-related restrictions in many states.

Year-to-date (YTD) margins increased and volumes continued to decline, while revenues and expenses rose across most metrics compared to the first three months of 2020. Year-over-year (YOY) margin increases were particularly pronounced. Those gains, however, are largely due to measuring March 2021 performance against the same period last year, when hospitals were hit with devastating losses from national shutdowns and halting of outpatient procedures during the first month of the pandemic.

COVID-19 cases and hospitalizations rose even as new vaccine doses surpassed 3.5 million per day in late March. The number of new COVID-19 cases was 50,681 on March 1, and increased 37% to a high of 69,551 on March 31, Centers for Disease Control and Prevention data show. New hospital admissions of patients diagnosed with COVID-19 increased 17%, from 4,610 on March 1 to a monthly high of 5,396 on March 30. To help illustrate the spread of variants, the prevalence of the U.K. COVID-19 variant B.1.1.7 rose to 45% of U.S. cases for the two-week period ending March 27, up from 12% for the two weeks ending Feb 27.

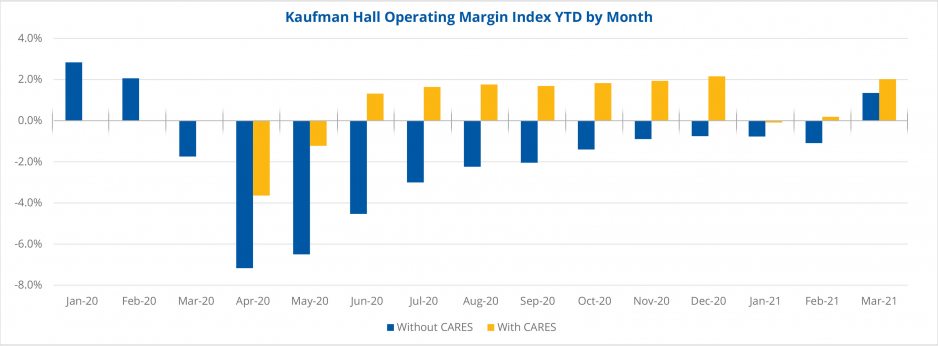

March hospital margins remained narrow. Not including federal CARES funding, the median Kaufman Hall hospital Operating Margin Index* was 1.4%. With the funding, it was 2.0%. The median Operating EBITDA Margin was 5.7% without CARES and 6.5% with CARES.

Hospitals saw gains across many key performance metrics, due in part to increasing outpatient activity. Without federal CARES funding, Operating Margin increased 34.5% or 2.5 percentage points YTD, and 69.5% or 5.2 percentage points month-over-month (MOM). Operating EBITDA Margin increased 20.7% or 2.2 percentage points YTD, and 39.6% or 4.3 percentage points MOM. Compared to the poor performance during the first month of the pandemic, Operating Margin jumped 128.4% or 14.5 percentage points YOY and Operating EBITDA Margin rose 148.1% or 13.3 percentage points YOY without CARES.

With CARES, Operating Margin increased 45.7% (3.2 percentage points) YTD and 61.1% (4.9 percentage points) MOM, while Operating EBITDA Margin rose 32.3% (3.0 percentage points) YTD, and 34.9% (3.8 percentage points) MOM. Compared to March 2020, Operating Margin increased 130.3% or 14.8 percentage points YOY, and Operating EBITDA Margin jumped 151.1% or 13.5 percentage points YOY with CARES.

Volumes decreased across most metrics YTD, but increased compared to especially low volumes in March 2020 and compared to a shorter month in February 2021. Discharges were down 8.2% from January to March compared to the same period last year, but increased 1.8% YOY and 12.7% MOM (1.6% MOM on a daily adjusted basis). Adjusted Discharges decreased 7.4% YTD, but rose 11.9% YOY and 20% MOM. Adjusted Patient Days fell just 0.8% YTD, but increased 17.2% YOY and 14.6% (3.1% on a daily adjusted basis) above February levels. Average Length of Stay rose 8.3% YTD and 4.1% YOY, but was down 4.3% compared to February.

Emergency Department Visits continued to see declines, falling 19.2% YTD and 3% YOY, but increased 20.3% MOM (8.2% on a daily adjusted basis). Operating Room Minutes rose 3.1% YTD and 21.1% MOM (9.7% on a daily adjusted basis). While surgery volumes remain down compared to pre-pandemic levels, the increases suggest that concerns over possible exposure to COVID-19 are easing as fewer people opt to delay non-urgent procedures. Year-over-year, Operating Room Minutes jumped 43.9% compared to March 2020, when many outpatient surgery services were cancelled due to the shutdowns.

Gross Operating Revenue (not including CARES) rose 4.4% from January to March compared to the same period last year, 24.8% YOY, and 16.8% MOM. Inpatient (IP) Revenue rose 3.7% YTD, 13.0% YOY, and 10% MOM. Outpatient (OP) Revenue was up 3.8% YTD, 31.6% compared to low OP Revenue in March 2020, and 21.4% compared to a 28-day month in February (9.6% on a daily adjusted basis). Adjusted for March’s volume levels, Net Patient Service Revenue (NPSR) per Adjusted Discharge increased 16.8% YTD and 12.2% YOY, but decreased 4.7% MOM. NPSR per Adjusted Patient Day rose 8.3% YTD, 8.0% YOY, and just 0.6% MOM.

Expenses increased across most metrics and measures in March, reflecting the continued high costs associated with the pandemic. Total Expense, Total Labor Expense, and Total Non-Labor Expense all increased about 4% YTD, while Total Expense per Adjusted Discharge, Labor Expense per Adjusted Discharge, and Non-Labor Expense per Adjusted Discharge all increased about 15% YTD. Looking at YOY and MOM results, total expenses increased while adjusted expenses decreased across most metrics. For example, Total Expense was up 7.0% YOY and 7.8% MOM, while Total Expense per Adjusted Discharge decreased 4.2% YOY and 10.6% MOM due to the increased volumes from February.

In the broader economy, the Consumer Confidence Index soared to its highest level since the beginning of the pandemic, up to 109.7 from 90.4 in February. The job market outperformed analysts’ estimates with a 916,000 increase in nonfarm payrolls, and the unemployment rate fell to 6.0%. During the Federal Open Market Committee’s mid-March meeting, Chairman Jerome Powell shrugged off inflation concerns. He reiterated the Fed’s intentions to support the economy through retaining near-zero rates and asset purchases of $120 billion per month. Market inflation fears resulted in a selloff of government bonds and a dip in equity markets in mid-March that impacted tech stocks especially hard. Equities have since recovered.

Upcoming issues of the National Hospital Flash Report likely will show continued margin and revenue gains, especially in comparison to record-poor performance in the early months of the pandemic. While some gains can be attributed to returning patient volumes, the impacts of the pandemic are far from over. Kaufman Hall forecasts the lingering effects of COVID-19 could drive 2021 hospital margins down 10% to 80%, and 2021 revenues down $53-$122 billion compared to pre-pandemic levels. One-third to one-half of U.S. hospitals may have negative operating margins by year’s end as a result

Kaufman Hall is pleased to introduce the Physician Flash Report, featuring insights on current industry trends with national data from nearly 100,000 providers from Axiom Comparative Analytics from Syntellis Performance Solutions. Read the quarterly report here.