Cash and investments play a number of important roles for not-for-profit healthcare, ranging from creating a credit profile that defines access to outside capital to buffering organizations from the variables and uncertainties of the changing business environment. Clear articulation of the deployment expectations of cash and investments will significantly impact each organization’s “optimal” approach to their allocation and management. Whereas many organizations historically have managed their cash and invested assets in a separate silo, healthcare’s rapid change is stressing this approach and, instead, encourages integrated decision support and management with the other risk- and-return pillars of the enterprise: operations, strategic initiatives, capital spending, and liabilities.

The Benefits of Liquidity

Not-for-profit health systems nationwide maintain $361 billion in invested assets, amounting to 66 percent of their annual revenue. The median cash holdings for the top 50 highest-revenue healthcare systems is $3.5 billion; in comparison, median cash holdings for the 50 largest private higher education institutions, which typically focus significant governance resources on investment management, is $2.5 billion.1

The higher cash buffer is maintained by healthcare organizations for good reason. Chief among these is the complexity of the credit model and the fact that the health systems have limited control over a significant portion of their revenues, which are tied to state and federal payment for patients covered by Medicaid and Medicare. Control or influence on the commercial side is increasingly difficult as well, as payers scale up and consumer expectations shift, escalating the migration of services to ambulatory and retail settings.

Cash has been key to fueling continued growth and stability during periods of significant shock. In recent decades, examples include revenue/operations pressures created by the Balanced Budget Act of 1997 and the balance sheet calls on capital to address bank bonds and fund-swap collateral demands during the 2008-2009 credit crisis.

For-profit healthcare and other public companies do not maintain excess cash at the levels seen by their not-for- profit counterparts since it dilutes return on investment for equity holders, who typically focus on the use of cash for operations. But for not-for-profit organizations, returns on sizable cash holdings have a significant impact on bottom lines and overall financial profiles that enable continued credit access.

Approaches with Invested Assets

Responsible cash stewardship in not-for-profit healthcare involves putting idle cash to work through capital market investment opportunities. But with investment comes uncertainty. A carefully crafted investment policy statement (IPS) is intended to define the parameters of investment. However, common objectives and constraints outlined in an IPS may inadvertently introduce an unsuitable role for investments. For example, an overly aggressive return objective, perhaps defined in concert with a financial plan, may lead an organization to “chase returns” and potentially introduce a higher-than-appropriate level of risk related to liabilities, operations, or strategic imperatives. The intended role of invested assets relative to the greater enterprise has repercussions for policy, strategy, and implementation.

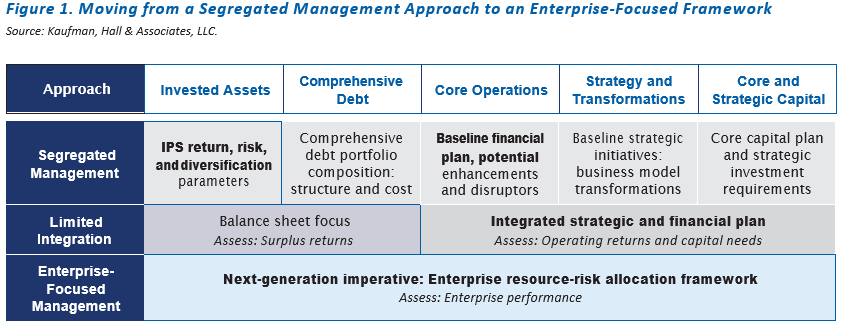

Consider three common approaches to managing invested assets in healthcare today (Figure 1).

Under a segregated management approach, investments are handled independently from operations or liability enterprise concerns, much like an endowment. This may be a popular approach, but often it is problematic due to the resulting lack or limitation of communication at the board/committee level between strategy, financial planning, and investments as well as with external financial advisors. These problems introduce vulnerabilities, mostly in the form of potential imbalances in the relationship between total enterprise risk versus the capacity of available risk-bearing resources.

A balance sheet-focused approach to invested asset management, used by a limited number of organizations, focuses on the integration of invested assets and the liability portfolio. Its main focus is the interplay between the two, especially creation of surplus return—i.e., investment earnings less interest expense. This approach introduces the idea of risk balance, but it limits the analysis to balance sheet resources. Consequently, there is no material insight on the operating and strategic activities of the enterprise. Because full enterprise risk balance is not considered, decisions are made without foundational context and often come down to preferences of investment committee members rather than overall organizational risks and resources.

An enterprise-focused management approach looks across the organization for the broad role cash plays in relationship to operations, strategy, and liabilities. Within operations, key factors include daily liquidity and working capital, intermediary obligations, and excess cash for capital funding. Simultaneously, this approach aims to facilitate balanced growth and income from invested assets while buffering assessed operational and balance sheet risks. Further, the approach is mindful of key duties of cash, involving the preservation of credit ratings and funding access, coverage of demand debt, and maintenance of liquidity covenants. Under this view, invested assets serve many roles and should continuously serve as the balancing agent for resources and risk across the enterprise, given their adjustment capabilities compared with other risk-bearing pursuits of the organization.

In times of stability, segregated management or balance sheet management of invested assets may be fine for an organization. But in times of change and high resource scarcity, reflected in today’s environment, an integrated, enterprise approach offers a better economic foundation for any healthcare organization. This approach ensures balanced value from all assets, aiming for a suitable return in view of their duties related to operations and debt strategies.

Defining the Role of Invested Assets

All organizations would benefit from articulating the role of invested assets and how they are managed across the enterprise in relationship to debt and operations. The degree to which investments are tied to the greater balance sheet and enterprise will impact the following, at a minimum:

- Alignment of the treasury team: The role of invested assets often helps clarify the proper role and guidelines for outside parties, such as investment and debt advisors

- Communication and reporting: The investment team will need to communicate with other areas of the enterprise. Cross-team interaction will help align invested assets with financial planning, debt, and clinical or strategy teams across operations

- Governance/committee focus: The structure of meetings and their agendas and frequency differ by approach. With the integrated approach, agendas typically focus on strategy and overall impact to the enterprise; under the segregated approach, investment manager selection and oversight often are prevailing investment committee topics; and under the enterprise-focused approach, agendas focus on all organizational risks and resources

Identifying a practical and appropriate cash investment policy that serves to accurately reflect the invested asset philosophy can be of great benefit to the overall enterprise. When articulated in a way that reflects the true goals of an organization, the full breadth of expectations is known to the investment execution team. This team maintains a thorough catalog of various cash pools and their accompanying objectives and restrictions. With expectations in place, governance and leadership feel less need to micromanage.

An example of a well-articulated process and policy for invested assets follows.

Invested Assets Example

A health system with revenue of $2.5 billion and Kaufman Hall developed a framework to support investment resource deployment in a risk-adjusted, integrated enterprise context. Using enterprise resource allocation, the framework tied organization-wide planning efforts with overall treasury functions, including capital funding, cash and credit management, external financing, and invested asset development and management.

A comprehensive report framed the overall goals and ongoing processes and set parameters going forward. Involving management and external advisors and shared with governance, the report clearly defined the rules for investment deployment. This helped focus conversations across governance, leadership teams, and external advisors on opportunities, challenges, and changes in the context of the framework. It included a catalog of available and realized resources (resource map) and potential cash requirements across the enterprise; a risk map reflecting shifting initiatives or liquidity pressures; defined liquidity tiers; and asset allocation structuring.

Cash and investable assets were divided into funds representing functional tiers linked to the greater enterprise. Each tier had a specified, agreed-upon purpose, defined volatility and liquidity parameters, return objectives, preliminary allocations, and other criteria. While studies often show that asset allocation typically accounts for more than 90 percent of nominal returns,2 here the sizing of fund tiers, which reflected distinct investment allocation strategies, had the greatest impact on returns.

Significant focus was given to sizing each tier for cash and liquidity as well as the sizing of intermediate funds to address scheduled and contingent events. The remaining assets fell into the long-term tier, which was constrained mostly by overall portfolio policies. These policies were described in detail separately for the health system.

Based on a clear picture of what the system wanted, leaders considered the engagement of an investment advisor who could deliver on that vision. After careful deliberation, the health system opted for an outsourced chief investment officer (OCIO) who would have discretion over day-to-day investment implementation and influence on the system’s overall strategy and key constraints, including tailored, socially responsible investing parameters. A revised IPS for the health system firmly put into practice the tailored viewpoint and constraints.

New processes are now in place that assure good communication and documentation across the team, both for routine matters, such as asset allocation rebalancing and any large payments that warrant liquidity planning, and for episodic issues, such as changes to the underlying assumptions in the integrated risk framework.

Concluding Comment

Cash investment must be judged by more than returns alone. A contemporary invested-asset strategy has a deeper, more complex purpose of facilitating the enterprise it serves. The approach for invested assets should embody organization-wide decision making by governance and cross-functional management. This creates clear alignment of the organization’s resources, its pursuits, and the team responsible for execution of the invested-assets strategy. Effective stewardship of invested assets within an integrated enterprise framework safeguards this important organizational resource, thereby empowering the organization and enhancing its ability to achieve its goals.

References

1Moody’s Municipal Financial Ratio Analysis database, 2016 audit data (accessed Dec. 8, 2017).

2Xiong, J.X., Ibbotson, R.G., Idzorek, T.M., and Chen, P., “The Equal Importance of Asset Allocation and Active Management,” Financial Analysts Journal, 66(2):22-30, Mar/Apr 2010.