Healthcare organizations have been under enormous pressure to operate with greater financial discipline. Most nonprofit healthcare systems devote significant time and energy to capital planning, debt capacity management, and long-term financial strategy. Decisions around facilities, major IT platforms, and long-term investments are typically evaluated through a rigorous financial lens.

Equipment, however, often sits just outside that discipline. In many organizations, equipment decisions begin with a clinical or operational need and move quickly into procurement. Only later, often very late in the process, does the question of how to pay for the equipment come into focus. Cash, leasing, or debt decisions are frequently made on a one-off basis, influenced by vendor offerings, timing pressures, and historical precedent rather than by a deliberate, system-wide strategy.

Yet, equipment represents recurring and material use of capital, with predictable replacement cycles and meaningful balance sheet implications. Over time, treating equipment finance as an afterthought leads to inefficient use of cash, misaligned financing terms, and reduced flexibility at a time when tight margins require capital discipline more than ever.

Starting from first principles: cash versus financing

A proactive equipment finance strategy begins with the decision to purchase an asset with cash or finance it in some way. Paying with cash simplifies execution and avoids interest expense, but it also draws directly on liquidity and reduces optionality. In today’s environment marked by tighter margins, normalized liquidity levels, and rising capital costs, those tradeoffs deserve careful consideration.

Financing is not inherently better than paying cash, nor is it always appropriate. When executed thoughtfully, financing can be a useful strategic tool. The key is to ensure that financing decisions are made intentionally and early, rather than reactively and by habit.

Figure 1. The broken status quo

Healthcare organizations can experience some or all of these structural challenges. None of these issues are dramatic on their own. Over time, however, they can compound.

|

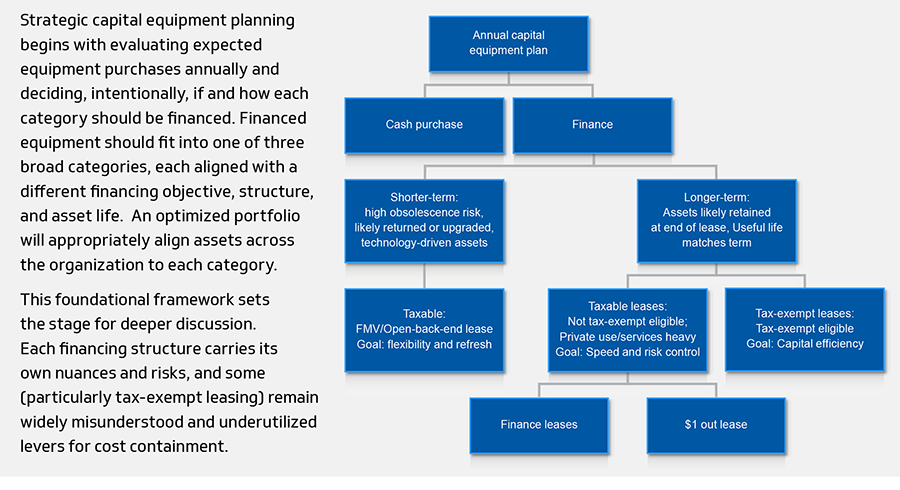

Equipment finance as a portfolio decision

A more disciplined approach treats equipment finance as a portfolio-level decision, evaluated annually and in aggregate alongside broader capital planning. This allows organizations to align financing choices with asset characteristics, liquidity goals, and balance sheet strategy rather than making isolated decisions under time pressure.

Figure 2. An annual capital equipment portfolio planning framework

Fair market value (FMV) or leasing

Flexibility matters more than ownership for equipment that carries a high risk of technological obsolescence or rapid performance evolution. This is particularly true for imaging, lab automation, and other technology where upgrade cycles are measured in years, not decades. The ability to upgrade, refresh, or return equipment at the end of term can be more valuable than locking in long-term financing or cash purchasing.

FMV or open back-end leases can support this objective by transferring residual value risk and facilitating predictable refresh cycles. When structured thoughtfully, these arrangements can help systems avoid being anchored to aging technology while maintaining operational continuity. The best outcomes in these arrangements are highly dependent on structure and rely on health systems driving terms of the master lease agreement with clearly defined end-of-term economics up-front.

Taxable finance leases

Taxable finance leases (also known as finance / $1 out leases) can offer speed, simplicity, and risk containment for assets that organizations expect to retain for their full useful lives but may not be appropriate candidates for tax-exempt financing. This may be due to private-use considerations, meaningful software or services components, execution complexity, or timing constraints.

These structures provide greater certainty than their FMV counterparts and more administrative efficiency when tax-exempt eligibility is unclear or impractical. It is important to note that while all $1 out leases are finance leases, not all finance leases are $1 out, so it is critical that the system ensures that the lease is structured properly to avoid costly back-end surprises.

Tax-exempt leasing

Qualifying entities often take advantage of tax-exempt leasing for large bond issuances but often overlook this financing option for capital equipment. For equipment that clearly meets tax-exempt financing requirements, such organizations can benefit from aligning financing terms with asset lives while preserving liquidity and avoiding the use of long-dated bond debt for shorter-lived investments.

Functionally, such leases often serve the same purpose as taxable $1 out leases, but at a materially lower cost, often on the order of When used selectively, tax-exempt leasing can complement a system’s broader debt strategy and improve overall capital efficiency without increasing structural complexity.

Why this matters now

The capital environment facing nonprofit healthcare systems has changed. Liquidity is no longer abundant, the cost of capital is structurally higher, and equipment portfolios are growing more complex. In this context, equipment finance can no longer be a tactical afterthought but rather an extension of balance sheet strategy.

For healthcare organizations, this means that bringing greater rigor to how equipment is financed is an overlooked lever to contain costs and preserve flexibility and debt capacity for strategic investments. Just as importantly, it is another opportunity to ensure that capital decisions are made in support of clinical care and are aligned with long-term financial sustainability.