Hospitals and health systems had a difficult start to 2021 as declining volumes, falling outpatient revenues, and rising expenses contributed to significant January margin declines. The ongoing effects of COVID-19 propelled January’s poor results, but it was a mixed month in terms of COVID-19 metrics. Some key pandemic indicators peaked in early to mid-January, but tapered in the second half of the month.

COVID-19 related hospitalizations increased steeply starting in September 2020 through early January 2021, according to The COVID Tracking Project. They reached a high of 132,474 on January 6, but declined for the latter half of the month, falling more than 28% to 95,013 by January 31.

New daily hospital admissions of infected patients reached a national peak of 18,006 on January 5, but dropped 50% by the second week of February, Centers for Disease Control and Prevention (CDC) statistics show. Other national data also reflect positive shifts with vaccinations on the rise and the average number of daily cases declining from mid-January to mid-February. If the trends continue, they suggest an easing of COVID-19’s impacts following a devastating winter surge.

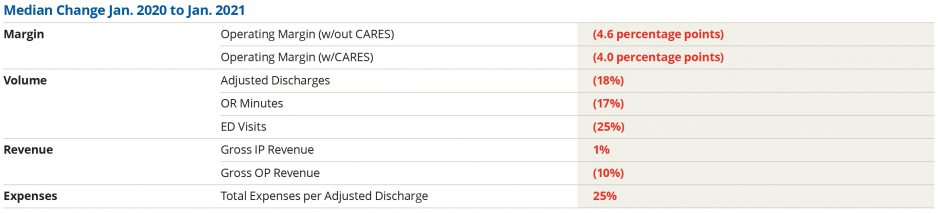

U.S. hospitals and health systems, however, face a long road to recovery, as January’s results illustrate. The median Kaufman Hall hospital Operating Margin Index* was -0.6% for the first month of the year, not including federal CARES funding. With the funding, it was -0.1%. The median Operating EBITDA Margin was 4.0% without CARES and 4.8% with CARES.

Not including the federal aid, Operating Margin fell 46.1% (4.6 percentage points) from January 2020 to January 2021, and Operating EBITDA Margin was down 34.1% (4.2 percentage points). Month-over-month, Operating Margin was down 26.7% (3.1 percentage points) and Operating EBITDA Margin declined 17.4% (2.3 percentage points) without CARES. Operating Margin fell 42.4% (4 percentage points) and Operating EBITDA Margin fell 25.4% (3.8 percentage points) year-over-year (YOY) with the federal aid.

Volumes were down across most metrics as many healthcare consumers continued to avoid or delay care out of concern for potential exposure to the virus. Compared to January 2020, Discharges dropped 12.7%, Adjusted Discharges fell 17.6%, Adjusted Patient Days declined 8.3%, and Operating Room Minutes fell 16.6%.

Emergency Department (ED) Visits again saw the biggest YOY volume drop at 24.7%, continuing a trend of double-digit YOY declines for the metric each month since March 2020. Inpatient volumes fell compared to January 2020—with Patient Days down 2.3%—suggesting a reversal following two consecutive months of YOY increases spurred by rising COVID-19 hospitalizations. Average Length of Stay (LOS) was the only volume metric to increase compared to 2020 levels, rising 12.6% YOY in January due to higher acuity patients requiring longer patient stays.

Revenue results for the month were mixed. Outpatient Revenue dropped 10.4% YOY in January, marking the ninth time it has fallen below prior year levels in the past 10 months. Lower outpatient revenues drove Gross Operating Revenue (not including CARES) down 4.8% YOY, while Inpatient Revenue rose slightly at 1.3% YOY. Revenues increased once adjusted for January’s low volumes. Net Patient Service Revenue (NPSR) per Adjusted Discharge rose 19% and NPSR per Adjusted Patient Day was up 9.7% YOY.

Expenses continued to climb across most metrics as hospitals remain encumbered by the high costs of labor, drugs, and personal protective equipment needed to treat higher acuity patients, including COVID-19 cases. Total Expense increased 4.5%, Total Labor Expense rose 6%, and Total Non-Labor Expense was up 2.4% YOY.

Looking at adjusted expenses, Total Expense per Adjusted Discharge jumped 25.4% YOY, largely due to a 30.1% YOY increase in Labor Expense per Adjusted Discharge. Full-Time Equivalents (FTEs) per Adjusted Occupied Bed (AOB) rose 6.1%. Non-Labor Expense per Adjusted Discharge rose 24.4% YOY, with the most significant increases occurring in Purchased Service Expense per Adjusted Discharge at 37% YOY and Drug Expense per Adjusted Discharge at 36% YOY. Overall Supply Expense was down just 1.5% YOY in January, but rose 19.9% YOY once adjusted to the month’s volumes.

In the broader economy, inflation and jobs data fell below expectations in January, as growth slowed considerably through the winter months. Stock values slid as trading driven by social media drew broad media attention, pushing the S&P 500 down 1.1% in January. The Federal Open Market Committee held steady at its January meeting and made no major changes to its guidance, keeping accommodative interest rates and asset purchase policies unchanged.

While national CDC metrics show some signs that the country may be turning the corner on the pandemic, its repercussions for the healthcare industry will persist indefinitely. The January performance results reflect the continued burden on U.S. hospitals and health systems, and emphasize the importance of remaining vigilant in combatting the virus and moving these vital institutions toward recovery.