The HIX Market Has Grown Rapidly; The Future Could Be (much) Bigger (or not!)

The Health Insurance Exchange (HIX) or Marketplace segment can be considered the largest growth market in the payer sector after Medicare Advantage (MA). From a relative low of 11.4 million members in 2020, the HIX market grew to 16.4 million members in 2023. In 2024, there are currently estimated to be more than 20 million HIX members, an expected compound annual growth rate of over 15%.

Several factors have contributed to this growth, including broader market and societal trends as well as favorable regulatory treatment. While some factors were intentionally designed to support HIX, others have indirectly served as a tailwind. Key drivers include:

- Ongoing employer frustration with cost and complexity of providing benefits, leading to employers gradually dropping coverage, especially true in small businesses (the percentage of firms with 3-49 workers offering health insurance has been in long-term decline from 64% in 2002 to 50% in 2023)

- The option for some employers to shift from regular employer-sponsored health benefits to ICHRA (Individual Contribution Health Reimbursement Arrangement) products over time, encouraging a shift to HIX plans (there was a 171% increase between 2022 and 2023 in the number of US workers offered ICHRA)

- Growth of entrepreneurs and gig workers (new business creation from 2015 to 2022 has gone from 2.8 million to 5 million), many of whom need a viable health insurance option

- Enhanced premium subsidies extended through 2025 in the Inflation Reduction Act that made HIX plans more affordable (in 2023, 14.3 million of all individual market enrollees were subsidized, compared to 9.2 million in 2020)

- Support from the federal government in the form of navigators (The Centers for Medicare & Medicaid Services (CMS) invested $98.6 million in grant funding to 57 returning Navigator organizations for the 2024 Open Enrollment)

- Recent unwinding of the Public Health Emergency and resulting Medicaid redeterminations prompting some individuals who no longer qualify for Medicaid to explore HIX as an alternative

- Emergence of the HIX market as America’s fallback option to get health insurance

While the recent HIX growth is exciting and has led to re-entry by several payers in the market, the forward growth trajectory is complicated to forecast, given inherent regulatory and market uncertainties, with large swings possible, both to the upside and downside. For example:

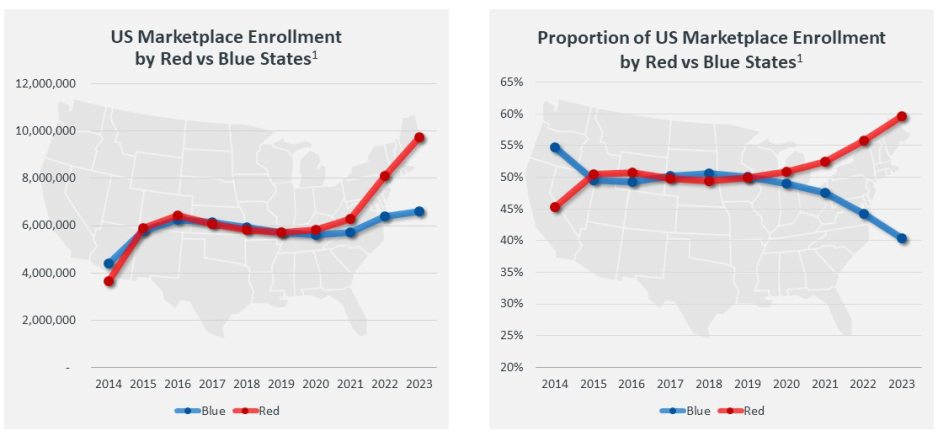

- Will the premium subsidies be extended beyond 2025? If so, the growth trajectory could continue; if not, could we see a stalling or even a potential shrinkage of the market? Per Figure 1, the number of HIX enrollees in “Red” states now significantly exceeds those in “Blue” states, providing some political risk mitigation from aggressive actions to devalue people’s HIX options

- When/will the remaining 10 states expand Medicaid, thereby shrinking the pool of lives that may seek HIX coverage?

- Will the employer market (especially small and mid-sized employers) tilt sharply in favor of ICHRA products that encourage a shift from traditional employer-sponsored plans to HIX plans, especially during periods of economic distress/recession?

Figure 1: HIX Enrollment in Red vs. Blue States

Source(s): Health Insurance Marketplace Open Enrollment Reports for 2014, 2015, and 2016, Office of the Assistant Secretary for Planning and Evaluation (ASPE), Department of Health and Human Services; Marketplace Open Enrollment Period Public Use Files for 2017-2023 Centers for Medicare and Medicaid Services (CMS), Department of Health and Human Services; CNN 2020 Presidential Results

Note(s): (1) Red and Blue States are defined as a state’s candidate outcome in the 2020 Presidential Election (i.e., Blue if Biden won and Red if Trump won)

An Options + No Regrets Hybrid Growth Approach

Given the market dynamics noted above, HIX payers can be imagined as riding a combination of two growth curves:

- A relatively steady growth curve driven by longstanding trends (e.g., gradual dropping of coverage, growing gig work).

- Another highly uncertain and volatile growth curve (or potentially negative growth curve) driven by sharp regulatory shifts and potential market dislocations.

So, how does a payer executive approach growth in such a volatile market? We suggest an options + no regrets growth approach as described below.

The no regrets part of this approach focuses on availing the relatively steady growth curve. This approach includes a range of tried-and-true organic growth initiatives in key functions, including product portfolio and metallic tier choices, product and network design, pricing, marketing, and distribution.

Further, payers have opportunities to micro-segment the market with tailored organic growth initiatives. For example, Legal Permanent Residents in the US, commonly known as Green Card (GC) holders, are eligible to buy health plans on HIX. About 1 million new GCs are issued every year. While 27% of GC holders get GCs through their employers, and presumably have access to employer-sponsored healthcare, 58% get GCs through their family. How many of these approximately 600,000 new family-sponsored GC holders buy on HIX and how should payers attract them?

Moreover, there are 12.7 million legal immigrants in the US that are eligible to buy plans on HIX. Eighteen percent of legal immigrants are uninsured, compared to 8% for US-born citizens. This 10-point gap in health insurance coverage raises the question of how to bring some of these approximately 1.3 million people into the HIX market. Exploring micro-segments like these and others will further organic growth for HIX payers. Add usage of AI and advanced analytics to identify leading indicators of an emerging prospect for the marketplace or switchers across HIX plans could further bolster these organic growth strategies.

Augmenting these no-regrets strategies, given the volatile growth curve of the HIX market noted earlier, payers can “buy” options to play this volatility, akin to financial markets where traders can buy options on securities based on their beliefs about the future. For example, payers assessing the business case for investing in their HIX business should consider the “option value” a strong HIX presence could create in the event of a disruptive event. For instance, an economic recession that accelerates the trend of employers dropping coverage or providing funds through an ICHRA could drive affected employees to seek coverage on the exchange.

This option value could be particularly interesting to regional plans that may feel societal and political pressure to stay invested in the HIX market, as it would improve their business case to stay invested. More broadly, given the fluidity of a portion of the population between commercial group plans, HIX and Medicaid, developing a presence in any of these segments is an option to gain exposure to the others.

Another example on the cost side is to develop strategies to account for variation in the payer administrative cost structure to a greater degree, to adapt to sharp shifts in volume. This could be accomplished through strategic internal reorganization and flexible deployment of resources and/or outsourcing to vendors for “surge capacity.”

A Word for Health Systems

While this blog is targeted to payers, in our connected healthcare ecosystem, developments in the HIX payer market can have significant implications for health systems. For example, while inflow from Medicaid to HIX may be margin positive, inflow from favorably reimbursed commercial group plans to relatively lower reimbursed HIX plans is likely to have a negative impact on margins. As discussed in our previous blog, health systems would be well-served to prepare for such an eventuality.

Conclusions

HIX is an exciting growth opportunity, and payers are jumping back in with understandable enthusiasm. However, the HIX market has some unique volatility, for which a different approach is advisable. This might include extending organic growth initiatives to micro-segmentation and targeting, and buying options to play the inherent market volatility.

Moreover, there is growing recognition of the strategic fluidity of the health plan market. Health plan members move in and out of group coverage, Medicaid and HIX over time, depending on their life choices and economic circumstances. Given this fluidity, HIX is emerging as America’s fallback insurance option—and thus worthy of a more strategic role in the portfolio of any payer.

The author would like to thank Brian Ball, Sarah Wiley, Yoram Levy and Webster Macomber for their insights and comments, and Rahul Tanna for his research and analytic support.