Healthcare issuance has been relatively modest over the past several weeks, with a mix of tax-exempt and taxable transactions across the credit curve. Transactions continue to get done at favorable levels but headwinds on rate volatility and fund outflows are creating more execution headwinds. Pre-marketing and thoughtful pricing tactics are important.

|

1 Year |

5 Year |

10 Year |

30 Year |

|

|

Feb. 11 – Treasury |

1.06% |

1.86% |

1.95% |

2.26% |

|

v. Jan. 28 |

+30 bps |

+24 bps |

+17 bps |

+18 bps |

|

Feb. 11 – MMD* |

0.78% |

1.34% |

1.61% |

2.03% |

|

v. Jan. 28 |

+17 bps |

+13 bps |

+6 bps |

+8 bps |

|

Feb. 11– MMD/UST |

73.6% |

72.0% |

82.6% |

89.8% |

|

v. Jan. 28 |

-7 bps |

-3 bps |

-5 bps |

-4 bps |

|

*Note: MMD assumes 5.00% coupon |

||||

SIFMA reset this week at 0.17%, which is approximately 137% of 1-Month LIBOR and represents an 11 basis point adjustment versus the January 26 reset.

Rising Rates and Market Risks

The Fed is poised to initiate a rising short-term rate regime at its March meeting. We hear from the capital markets community about the potential for as many as five to seven rate hikes over the near term. Debate continues about the possibility for a 50 basis point move in March, as well as any steps the Fed might take to accelerate the unwinding of its $9 trillion balance sheet.

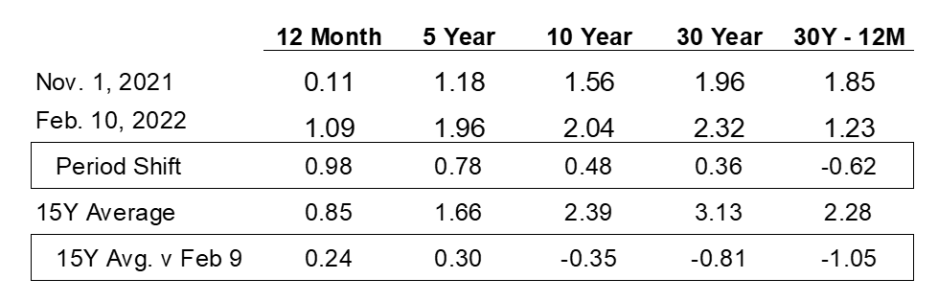

The fascinating part of all this continues to be the market response to known inflationary pressures (published year-over-year CPI increases) paired with the uniform expectations for significant monetary tightening. The table below compares Treasury rates and curve spread (30-year versus 1-year) on November 1, 2021, versus February 10, 2022, and then between February 10, 2022, and the 15-year average.

The response of fixed income investors to all the unsettling economic and monetary developments during the past several months has been curve flattening, driven by the shorter end moving up faster than the long end. During the measurement period, one-year Treasuries increased 98 basis points and 5-year Treasuries moved 78 basis points, and both ended well above their 15-year trailing averages; conversely, 10-year bonds were up 48 basis points and 30-years increased 36 basis points, and both remain below their respective 15-year averages. The result is the curve spread dropping from 185 basis points to 123 basis points, which is 105 basis points flatter than the post-credit-crisis average. Noteworthy was the Treasury market response to the Labor Department’s February 10 release of a 7.50% year-over-year increase in the Consumer Price Index (the highest increase in four decades): 1-year up 20 basis points, 5-year up 14 basis points, 10-year up 10 basis points, and 30-year up 4 basis points; additionally, the S&P 500, Dow Jones Industrial Average, and Nasdaq Composite all fell at least 1.40% on the day.

While long-term borrowing rates remain historically attractive, the overall rate trends—especially set against days like February 10—highlight the market risk confronting healthcare providers. If investor sentiment turns, the dislocation across all markets—equity and debt, traditional and alternative—will likely be significant. This will make the balance sheet—the anchor of resiliency and stability since March 2020—one more performance and credit headwind. Stopping asset purchases, which is scheduled to occur soon, will take away the primary lever the Fed has relied on to influence long rates; and any shift (or even hint) of accelerated liquidation of its balance sheet holdings is likely to create further dislocations. It is a remarkably concentrated and systemic risk that all revolves around the Fed’s ability to artfully withdraw enough of the liquidity it has injected into the system to get inflation under control.

There was an interesting piece in the February 9 Wall Street Journal by Daniel Altman, the chief economist of Instawork. The article addressed the various ways that workers tapping into flexible work platforms like Instawork or Amazon Flex or Trusted Health are reshaping (disrupting) traditional labor relationships. The whole labor dislocation thread is, of course, foundational to the staffing and expense challenges confronting healthcare providers. But the other idea that caught my attention was Altman’s suggestion that traditional government labor-tracking tools may not appropriately account for or capture many flexible workers. He suggested that perhaps “unemployment rates today aren’t strictly comparable to those of even a decade ago. Policy makers who care about unemployment, including the Federal Reserve, may have to recalibrate their targets.” As my colleague Terri Wareham says, “Yikes!”

The Fed poured liquidity into the world with the hope that balance sheets would mitigate a revenue-driven operating disruption (economic lockdown). Now the Fed will risk balance sheet stability to withdraw that liquidity with the hope of mitigating an expense-drive operating disruption (inflation). A troubling question for the healthcare sub-economy is whether the Fed can influence the sector’s most important expense disruption. In a “generic” labor economy, the Fed raises rates to dampen economic growth, which ultimately eases employment pressures, moderates wages, and cools inflation. But in a specialized labor sub-economy (healthcare and nursing), the worrisome scenario is that Fed rate hikes have no material impact on the demand (need) for services and, consequently, no impact on the demand (need) for the required skilled labor. In this scenario, the emergence of flexible work platforms like Trusted Health prove more impactful than Fed policy. If this is true, then the Fed playbook applied to healthcare might drive the credit and resiliency challenge of strong headwinds for investment returns but only modest tailwinds for operating costs (at least the skilled labor side of the cost structure).

A consistent theme of this series has been whether we are driving on new roads using out-of-date maps. The troubling thought is that this same possibility might extend to the Fed—but then would it really be surprising if all the disruptive forces upending corporate operations also wind up distorting the tools our central bank relies on to address the full employment part of its dual mandate? Risks abound and some are unsettling (closer to unknowns than risks); the best response continues to be thinking through scenarios and doing the work to position resources to create maximum resiliency.

Trending in Healthcare Treasury and Capital Markets is a biweekly blog providing updates on changes in the capital markets and insights on the implications of industry trends for Treasury operations, authored by Kaufman Hall Managing Director Eric Jordahl.